Taxes in Estonia in 2023-24

Estonia is a country located in Northern Europe, known for its business-friendly policies and low tax rates. The Estonian tax system is simple and transparent, making the country an attractive destination for foreign investors looking to set up a business.

The Estonian government has also implemented

several tax incentives to attract foreign investment and promote entrepreneurship, such as the exemption of reinvested profits from income tax and the reduced social tax rate for startups.

Additionally, Estonia has a unique tax system called the “zero tax” system, which means that companies are not taxed on profits that are reinvested back into the business. This has led to a culture of entrepreneurship and innovation in Estonia, which is why many startups and tech companies choose to set up their businesses in the Estonia.

Aside from the corporate tax, there are several other taxes that businesses and individuals must pay in Estonia. These include personal income tax, social security tax, value-added tax (VAT), and excise duties.

In this article, we will discuss the various taxes in Estonia which is imposed on the incomes of residents & non-residents. So, let’s dwell on it.

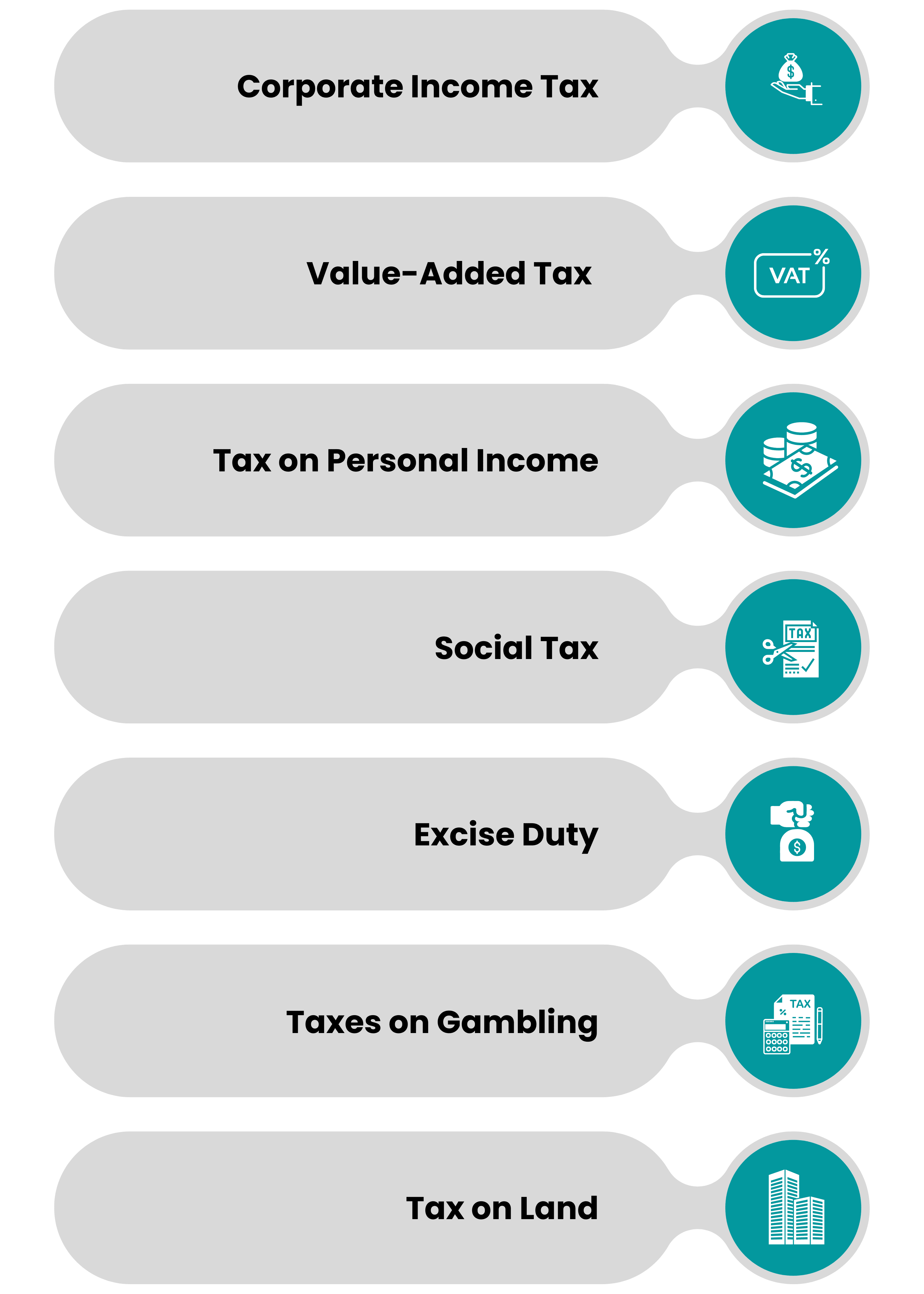

List of Numerous Corporate Taxes in Estonia

Down below, we’ve listed the numerous taxes in Estonia, which are imposed on incomes or multiple sorts of earnings.

Corporate Income Tax

| Tax Type | Tax Rate | Condition |

|---|---|---|

| Corporate Tax | 20% | Applicable to profits distributed as dividends or retained. |

| Value Added-Tax(VAT) | 20% | Applicable to most goods and services sold in Estonia. |

| Personal Income Tax | 20% | Applicable to employment and business income. |

| Social Tax | 33% | Applicable to employment income. |

| Excise Duty | Varies by product and volume | Applicable to specific goods, such as fuel and alcohol. |

| Taxes and Gambling | Standard tax is 5%, however, it can vary by game and revenue. | Applicable to revenue earned from gambling activities. |

| Taxes on Land | 0.1% to 2.5% | Applicable to the value of the land owned. |

In the wake of reforms, the most significant advantage for entrepreneurs was the exemption from corporate tax on income in the case of investing profits.

Therefore, Estonian businesses are required to pay tax only on the distribution of their profits, which is dividends. Corporate income tax (tax on dividends) is 20% percent of dividends earned.

The taxation system differs conceptually from the traditional income tax system since the tax is assessed on the distribution of profits (also hidden distributable earnings) instead of the profits of the company.

Value-added Tax (VAT)

The value-added taxpayers are companies whose taxable supplies (except import) do not exceed EUR 16,000 over one calendar year. The tax is imposed on transactions involving products and services within Estonia as well as on imports of products. Tax rates are 20% of the value that is taxable.

Every month, the state budget must receive the value-added tax by the 20th. The tax is paid in full to the budget of the State.

The process of registering companies is done via the Tax and Customs Board which also manages the tax on VAT imposed on the import of goods and services.

Tax on personal income

Taxes on personal income are 20% of taxable income, and residents are required to pay tax on the income they earn in and out of Estonia.

The taxable revenue comprises earnings from work (salary pay, wage bonus, payments) as well as business income, rent, interest, royalties, capital gains, pensions, maintenance support, and scholarships (except for scholarships funded by the state budget or according to the law).

Social Tax

The tax is used to provide state pensions as well as health insurance. The tax can be paid by legally constituted entities as well as natural persons and non-residents who earn a regular income.

It is taxed at 33% of the amount taxable. The tax is calculated monthly and an equivalent amount of money has to be paid out by the tenth day of every month.

Since January 1, 1999, social tax payment has been personalized and made up of pension funds, which are considered in every particular instance. The tax is stored in a specific savings account for health insurance and pensions that are part of the budget of the state.

Excise Duty

The Estonian government charges excise duty on liquor, tobacco, fuel, packaging, and automobiles.

The tax helps limit the quantity of a specific item or to provide a specific service to help adjust the amount of consumption for domestically-produced products.

Tax revenues from VAT, as well as excise duty revenue, are affected by changes in demand in the domestic market and the increase in the imports of goods that are excised as well as adjustments in rates for excise duties.

Tax on land

It is 0.1-2.5% of the taxable value. The tax for land on which economic activity is prohibited is established through the determination of government officials of the Estonian government, which is in the amounts of 25%, 50%, or 75% of the tax rates.

The land tax is paid three times per year – at the time of 15 April, 15 July, and 15 October.

The land tax is payable on any land, excluding:

- The place in which economic activity is not permitted

- The land that is adjacent to buildings or portions of them, which are diplomatic missions or consular representations from foreign states

- Cemeteries, and the land that is under the temples and churches of congregations

- Land that is owned by an international or foreign state organization. Additionally, the municipal tax is not imposed on land that is owned by the municipal government or on land that is located in public service. This is to the decisions that the city’s government makes.

The value of land is defined through the Land Valuation Act. Some exemptions include the taxes on the land for areas in cultivation, as well as natural forest and grasslands, which is 0.1 percent to 2.0 percent on the appraised value for the land each year.

Pensioners may be exempted from having to pay taxes on land up to 0.1 hectares in urban areas and 1.0 acres in rural municipalities under the assumption that the person applying for tax exemption is using the land to live and doesn’t receive rent based on the right to use the land.

Taxes on gambling

The gambling tax is imposed on the earnings from games of chance, betting, totalisators, and lotteries, as well as in the form of gambling tables and equipment that are used to organize games of chance at licensed venues. The tax is calculated based on payments made out of which winnings are made.

The taxable period for the organization of lotteries, games, and skill is a calendar month. The tax-free period for totalizers is the time during which the betting event is held (it must fall within the financial year in which it is held).

Tax rates are as follows:

- EUR 447 for each machine

- EUR 1278 for a table of gambling.

The rate of taxation for gambling is 5% on totalisators, 18% on skill gaming, and 18% on the lottery.

Conclusion

It’s important to note that businesses operating in Estonia still need to comply with various tax regulations and requirements, including registration for VAT and social security contributions.

With its competitive tax rates and business-friendly policies, Estonia remains an attractive destination for investors and entrepreneurs looking to establish a presence in the European Union.

If you are even considering registering a company in Estonia, you shoulD be aware of all the tax norms. It’s recommended that companies seek professional advice from Odint Consultancy to ensure they understand their tax obligations and are in compliance with all regulations.

FAQ’s

A 0 percent corporate tax rate is where you do not pay taxes on the income of your year and file no annual tax returns regardless of your profits or losses. Pay 0% tax on reinvested profits.

If the tax-deductible supplies of Estonian resident companies or the PE of a non-resident company located in Estonia exceed EUR 40,000 in one calendar year VAT registration is required.

For Estonia, taxes are deducted from your gross earnings through your workplace based every month. This means that you don’t need to pay additional taxes or file tax returns for each month.

The three primary income sources for federal taxes are a tax on individual income tax on payroll, individual income taxes, as well as corporate tax. Other tax revenue sources include excise tax, estate tax, as well as other taxes and charges.

Distribution of dividends can be subjected to 20 percent corporation tax (CIT) in Estonia and the recipient must declare dividends to the country in which their tax residence is as per the tax rate of their local jurisdiction.