What is a Dividend?

Any type of cash, reward, or any other thing that a shareholder receives through a company is called a dividend. The precise percentage of the corporation’s net profit that is distributed to the shareholders s a return on the shares they had subscribed for is known as a dividend. Dividends can be considered in different forms, like stocks, cash, and so on.

The decision on what the dividend would be is done by the company’s board of directors and the approval of the shareholder is required as well. But it is to be noted that a company is not liable to pay the dividend. To sum it up, the dividend is nothing but a profitable portion that a company distributes to its stockholders.

This article will examine dividends, the forms of dividends, as well as the advantages and drawbacks of declaring dividends.

Types of Dividends in India

Companies always look for ways they can generate increased value for their consumers through their services or products. To make that happen some amount of revenue is charged, which is known as the profit. So, if any firm is developing profit, it is their wish to reinvest that profit into businesses or they could distribute that profit to their investors as a dividend.

There are several ways a dividend can be distributed. The firm also has a choice to decide how frequently they want the dividend to be delivered. Meaning they can send it every month, year, or even quarterly. It all depends on what is the policy of the firm.

To learn more deeply, here are the different types of dividends:

- Stock Dividend

- Cash Dividend

- Scrip Dividend

- Property Dividend

- Liquidating Dividend

Stock Dividend

If any firm decides to deliver extra shares to its investors without any expectation, then that kind of dividend becomes a stock dividend. If the firm sets less than 25 percent of the old issued stocks, then it’s termed a stock dividend. And if the issued stocks are more than 25% of the old shares then it is coined as a stock split. An example to make it clearer is, if a firm declares 10K shares as dividend to its stakeholders, the fair value of the stock is Rs. 200, and the par value is Rs. 1, then the entry documented by the firm would be-

Retained Earnings – 50k Debit

Common Stocks, Rs 1 par value – 10K Credit

Additional paid-in-capital – 40K Credit

Cash Dividend

This type of dividend is the most famous kind of dividend. In this kind of dividend delivery, the firm delivers the dividend in the form of money to all the stakeholders depending on their holdings in the company. The company delivers the dividend in the bank accounts of the investors. There is a complete process for the declaration of dividends.

For example, a company decides with its directors to give out Rs 2 for every share of the firm’s 20L remaining shares to be given on 26th Jan to all stakeholders onboard by 10th January, and the documented entry on 1st January would be –

Retained Earnings – 10L Debit

Dividends Payable – 10L Credit

After 26th January, the investors will get the dividend in their associated bank account.

Scrip Dividend

This dividend is delivered when any firm is not able to generate the required funds to send out dividends. So, in this case, the company decides to deliver the dividend as a promissory note and pays its investors on another date.

Property Dividend

Any firm has the liberty to issue a non-monetary type of dividend amongst its investors. The decided property dividend is then documented as per the original price of the distributed asset. The market cost of the property is thought to be around the book value.

This decides if the firm will face a loss or profit, and an entry is made in the books accordingly. This analysis of the delivered property can force firms to issue this type of dividend intentionally to control the taxable pay.

Liquidating Dividend

This type of dividend occurs when the directorial board of a firm decides of sending back the actual capital put in by the stakeholders. This is a sign of a business getting wrapped up.

Insight on Dividend Distribution

Once the company completes its payments to the creditors, the amount of profit left is then distributed amongst the stockholders in the form of a dividend. It is the company’s choice to give spend half or whole profit. The sending out of dividends can be avoided if the company is running short on cash or needs it to complete reinvestments.

Once a dividend is declared by a company, a particular record date is marked. So, all the stockholders who are registered till that particular date become qualified to receive the dividend as per their respective shareholding.

Cheques through the company get mailed to the shareholders within a week, and the dividends get transformed into ex-dividends once 2 working days after the record date pass.

Those two business days are the only time when stocks can be easily sold or bought. Declaration of dividends according to a recent study it was found that companies paying dividends have reduced from 24% in 2001 to roundabout 16% in 2009 and rose to 19% in 2010.

Procedure for Declaration of Dividend as per Companies Act of 2013

The procedure through which the Directorial Board of a firm decides and declares a dividend for distribution to shareholders, reducing the firm’s retained earnings statement by the sum of the announced dividend.

The following information must be included in the dividend letter: The individuals eligible to partake in the payout must be notified of the declaration.

Note: According to Clause 87 of Model Articles of Company limited by shares as contained in Table-F of schedule-I of Companies Act, 2013.

According to the Companies Act of 2013, the method of declaring dividends is as follows:

1. The sum of dividends that the firm recommends to the General meeting is up to the team of directors to determine.

2. The decision for dividend must be stated in the Announcement of the General meeting by the firm.

3. The general meeting will be held by the firm:

- Normal Trade is the declaration of dividends.

- The meeting will decide if the declaration of dividends will get approved.

4. As the dividend is proclaimed, it should be distributed within 1 month.

Importance Points to Note

- The dividend announced in the General meeting must not be greater than the dividend proposed by the Management board.

- The dividend announced by a person in a General Meeting may be smaller than the Panel’s proposed payout.

- The Final Dividend is the dividend given at the Annual Meeting.

Companies Act, 2013 prohibits the declaration of dividends if:

- If a firm has default sections 73 and 74 relating to deposits and interest collection, it might issue or not issue a dividend.

- A firm cannot issue a reward if it refuses to adhere to the acquisition and reimbursement of deposits.

Penalties for failing to distribute dividends (section 127)

If a firm declares to pay a dividend but can’t pay it or is not able to publish the warrant for it in a month from the date of the declaration to the stockholders, so each director from the board of the organization shall be sentenced to two years in jail and a penalty of 1K starting from the day the default was committed. The corporation will be ordered to contribute simple interest at an ROI of 18 percent per annum for as long as the delinquency persists.

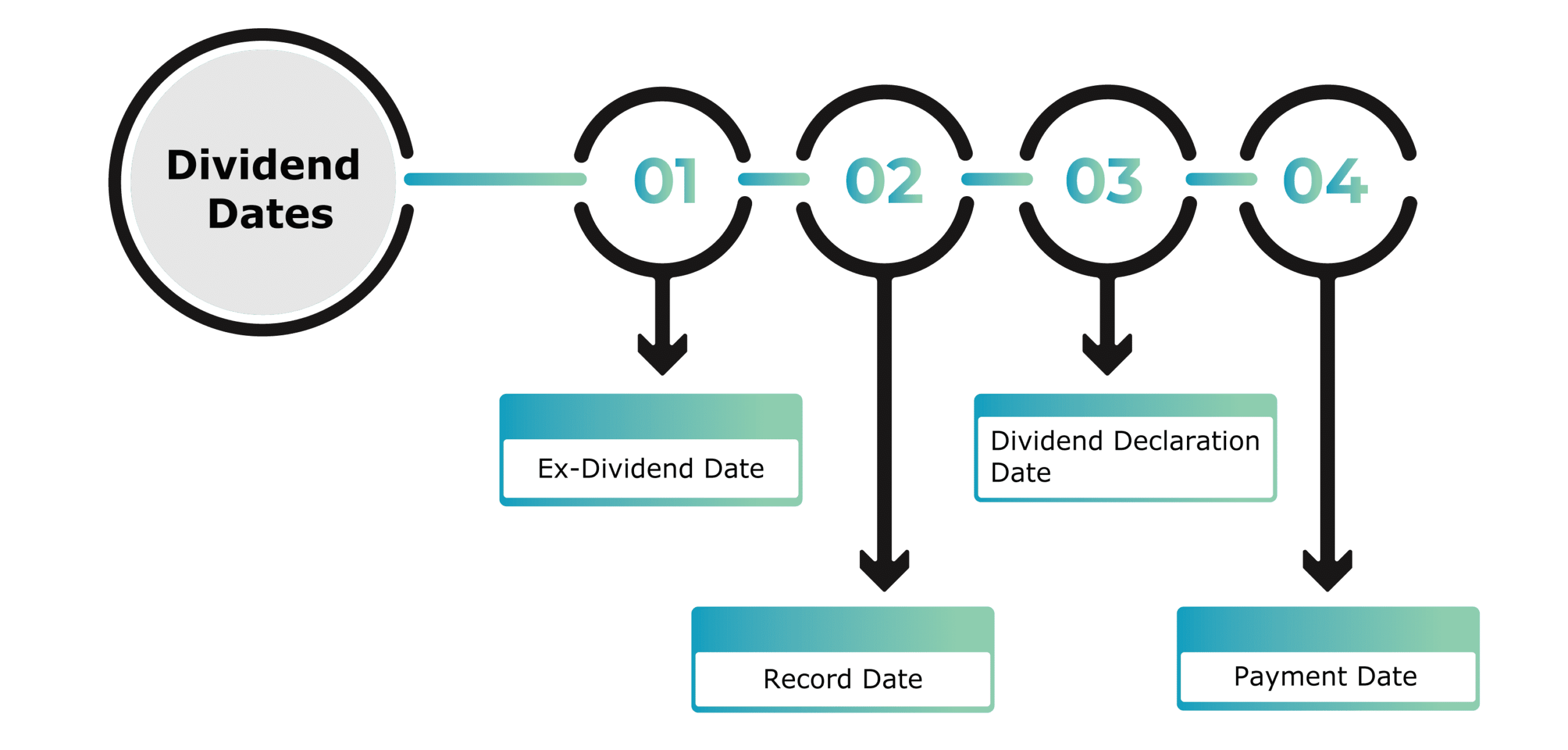

Dividend Dates

Evaluating dividend-paying equities necessitates knowledge of significant dividend deadlines. Typically, a reward is paid to shareholders in cash form from the firm’s earnings. A company could choose to distribute a reward to the investors instead of reinvesting revenues again into the organization. The most important factor in obtaining dividends is the period spent purchasing and keeping the stock.

There are four important Dividend declaration dates that every investor should know.

- Ex-Dividend Date

- Record Date

- Dividend Declaration Date

- Payment Date

Date of Expiration of Dividends: The ex-dividend deadline is the day when all newly bought and sold stocks lose their right to receive the most publicly claimed dividend. This is a significant day for any company with a big number of shareholders, especially those that participate in marketplaces because it makes deciding who will receive the dividend much easier.

Date of the Dividend Record: All investors whose information appears in the firm’s share registers as of the settlement date receive the reward. The time frame, also called the date of registration, is the deadline for registering an asset with the company in terms of getting a dividend.

Date of the Dividend Declaration: The company distributes dividends to its shareholders on this day. As the conference goes ahead, the date of dividend distribution, the amount of the reward, the quantity of dividends investors will receive for each owning share, and the settlement date all will be addressed.

Advantages of Declaration of Dividends

There are a lot of reasons why investors get intrigued by the thought of getting a dividend.

Some of the advantages are listed below:

Expansion & Profitable Growth

Dividends start to develop gradually over time, which is among the main benefit of putting money in dividend-supporting businesses. Dividend-paying corporations that have been around for a while usually boost their payments year after year. A handful of “dividend enthusiasts,” or businesses that have raised their dividend payments for even more than 25 years running, exist.

Dividends are beneficial when evaluating stocks

Investors frequently neglect the influence of dividends on the total rate of return, and also the notion that dividends represent a useful point of assessment in equity analysis and investment strategies. Dividends are a more dependable gauge of market valuation than several other commonly employed metrics.

Threat and Variability Reduction

Dividends play a big role in lowering asset volatility and risk. Dividend payouts, in the concept of risk reduction, offset any losses incurred as a result of a share price decrease. Dividend payouts, on the other hand, have a vulnerability prevention benefit that goes well beyond a simple fact.

Dividend-paying equities have typically outperformed non-dividend-paying equities during down-market periods, according to research. While a broad downturn lowers stock prices for consumers, dividend-paying equities typically lose less worth than non-dividend-paying equities.

Dividends provide tax benefits

Dividends are rather tax-efficient ways of getting revenue because of the manner they are regarded in terms of taxes.

- Dividends help to keep capital’s asset value

Disadvantages of Declaration of Dividends

- Dividends may help with another issue that many investors overlook: the impact of monetary policy on returns on investments. To get a real net benefit from a fund, the investment should first produce a sufficient return to offset the costs of purchasing power caused by inflation.

- The fact that firms run out of funds by dividend payments to owners is a significant constraint. This money might be better spent on business investments that would have resulted in more development. In this sense, dividend payments result in the corporation sacrificing long-term development for relatively brief gains.

- Dividends are distributed at senior management’s judgment. Businesses are not required to make these contributions. Even if the company makes a profit, the administration may opt not to pay a dividend.

Businesses must pay taxes on the sum of profit they are ready to give to their shareholders when they issue dividends. Dividends increase the firm’s tax liability in this manner.

What is the difference between Dividend Declared Vs Dividend Paid?

Investors and businesses need to be aware of the distinctions between the dividend declared and the dividend paid in order to fully appreciate the dividend declared’s meaning. Here are a few points where the two are different:

- A dividend is declared when the board of directors makes a statement about dividend distribution. The accounting impact of the dividend is preserved, the company’s earnings balance is decreased, and a temporary liability account with a value of the same amount is formed and referred to as “dividends payable.”

- The moment the investor’s account receives the dividends is known as the dividend paid. The “dividends payable” liability account is eliminated from the company’s balance sheet when the dividends are paid, and a corresponding amount is deducted from the cash account.

Conclusion

To declare a dividend and to send the funds to the bank account, the judgment of the board of directors is very necessary. There is no way you or anyone can question the decision made by the board. The dividend must get paid in 1 month to all the investors.

The Share or Stock Dividend is only given once the dividend of preferred stock is announced. The total sum of the dividend, including the interim dividend should be transferred to a separate bank, and in a separate account. This transfer should be completed in 5 days, starting from the date of declaration of this type of dividend.

If you want to know more about the declaration of dividends in more in-depth, you must seek assistance from professional experts from OnDemand International. Contact us.

Read About: Allotment of shares

FAQ’s

The income statement does not include dividends. Once declared, they would appear in a statement of retained earnings or a statement of stockholders’ equity, and when paid, they would appear in a financing activities.

A dividend yield is just a ratio between the amount of dividend to be paid per share and the market price that the share is being traded for at a fixed point of time.

A dividend yield is different from the Earnings per share – which is the ratio between the total profit and the total number of shares of the company.

A dividend is a token premium reimbursed to the shareholders or majority stakeholders for their income in a corporation’s capital, and it usually occurs from the firm’s gross income. While the important fraction of the profits are kept within the firm as a retained dividend which exemplifies the money to be utilized for the firm’s continuous and future company activities—the remainder can be allotted to the shareholders as an income.

At times, firms may still give away dividends even when they don’t make acceptable revenue. They may do so to retain their traditional track record of giving rise to legal dividend incomes.

The board of directors of a company has the authority to announce dividends.

A final dividend is a dividend suggested by the directorial board and announced by the participants at a yearly General Meeting.