Overview: Ways To Improve The Debt To Asset Ratio of a Company

The debt-to-asset ratio is a financial ratio that is similar to the liabilities proportion. The debt-to-total-asset proportion is a liquidity ratio that compares a firm’s revenue obligations to its asset value. It is determined by dividing a company’s overall debt, or total outside obligations, by the entire resources used in the firm. It’s sometimes just referred to as financial leverage. A corporation often uses stock and loan financing to inject certain funds into the organization. It’s crucial to know how much of a firm’s capital is contributed by debt rather than equity.

The debt-to-asset ratio expresses the debt’s organizational investments concerning the firm’s profits. A massive debt ratio might contribute to the company’s erratic development and undermine investors’ faith in the offshore company. The debt ratio also indicates how a business has grown and amassed assets over time.

This article explains how to analyze and interpret this formula so that it may be used to make informed business decisions. This ratio attempts to assess how many of the firm’s profits should be auctioned off the firm’s outstanding liabilities.

Relevance of debt to asset ratio

Under all circumstances, a firm should make commitments to existing debt. Otherwise, the company will default on its loan agreements, putting it in danger of being forced into insolvency by investors and other stakeholders. Other commitments, such as accounting records and protracted contracts, may be settled and bargained to some level, but debt contracts have very limited room for flexibility. As a result, a company with a high level of leverage may find it more difficult to stay afloat during a crisis than one with a moderate leverage ratio. The debt-to-asset ratio is a useful metric for ensuring an organization’s ultimate economic health.

The following are some of the key factors that demonstrate the meaning and benefits of the debt to asset ratio:

- The larger the amount of borrowed funds the bigger the danger of engaging in the firm, and the higher will be the debt proportion.

- The method is used by lenders to analyze if a company has sufficient finances to pay its outstanding debt obligations and whether it will generate a profit.

- This assessment considers all of the firm’s commitments, not simply those payable on borrowings, as well as any unsecured resources and intangible property.

- The ratio helps to compare the debt rates at different businesses. Researchers may compare a corporation’s economic performance to that of other firms in the same sector. The data might reveal a company’s financial stability.

- The computation is something that researchers evaluate when analyzing the worth of a possible acquisition since it serves as a foundation for a corporation’s economic state.

- It offers insight into a company’s financing practices and, as a result, focuses on the strategic and long financial status.

- This metric provides an indication of a business’s performance as well as the proportional debt and equity borrowing ratios.

- The debt-to-asset ratio indicates the percentage of asset that are funded with debt, and hence the degree of financial strain.

- It is used to evaluate a company’s budget deficit to its entire assets, which includes both assets and liabilities funding, or to the net capital utilized in the organization.

General Practice

The practice of showing liabilities as a numeric approximation of the ratio of the total assets is widespread. The proportion might swing from 0% to 100% in terms of percentage. Any value larger than one indicates that a firm is lawfully bankrupt and poses substantial financial dangers, that is the organization seems to have more obligations than resources. It means that a significant amount of the assets are financed by borrowing, and the firm is at a greater financial risk. As a result, the lower the value, the healthier the company is.

A debt to asset ratio of 0.5 indicates that debts fund half of the firm’s assets. To put it another way, borrowing only accounts for half of the total capital. Likewise, if a firm’s revenue solvency ratio is 0.4, lenders finance 40% of its resources while proprietors fund 60%.

A lesser ratio value appears to be preferable to a higher proportion. This is due to the fact that a lower number indicates a solid corporation with fewer debt loads. A greater ratio, on the other hand, suggests that the business’s creditors can claim a larger share of the assets. As a result, there would be a more operational risk as new projects will be tougher to fund. The higher your debt-to-asset ratio gets, the more you owe and the more danger you’re taking on by taking on more credit lines. As a result, it is generally suggested that enterprises with a greater debt-to-asset ratio seek equity capital.

Necessity to improve the debt to asset ratio

A greater debt-to-asset proportion is unfavorable for a business. The preceding are some of the chief factors why a company should aim to change its debt-to-asset ratio:

- To begin with, it implies that a more significant proportion of capital is contributed by debt.

- A more significant percentage increases the difficulty of obtaining funding for future business advancements since creditors may perceive the firm as an unpredictable or dangerous investment.

- In addition, a larger debt-to-asset proportion raises the chance of bankruptcy. If the firm is dissolved, the resources may not be sufficient to pay off all existing debts.

It’s usually a good idea to maintain debt minimal in order to maintain the financial leverage stable and guarantee that the existing commodities are adequate to pay off the loans.

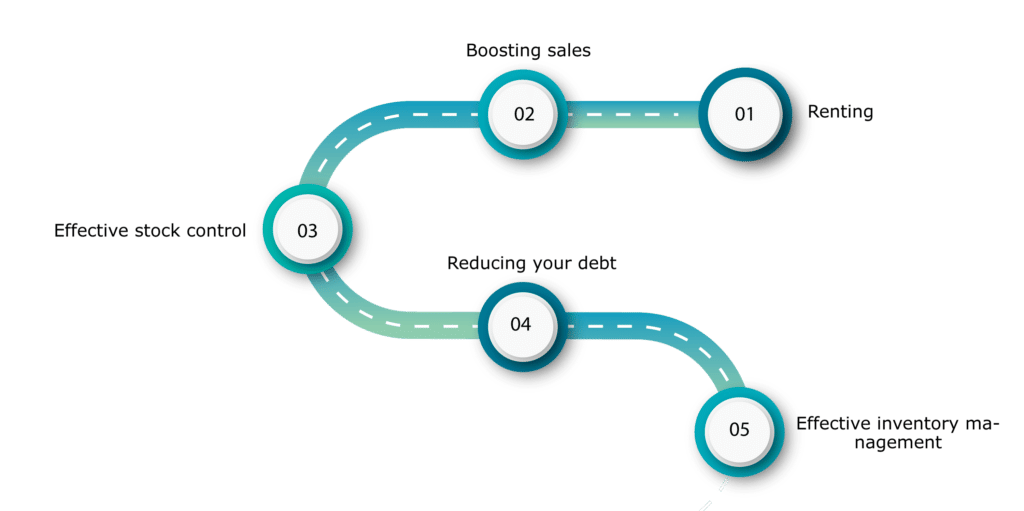

Ways to improve the debt to asset ratio of a company

If a company’s debt to asset ratio as determined by its banking statements is excessively high, it must lower it. To put it simply, the corporation should reduce its debt percentage to reduce the proportion. However, there are a variety of additional techniques to enhance the debt-to-asset proportion, some of which are included below:

Renting: A business sells its resources and then re-lease its buildings. This will lead to an increase in retained earnings that may be used to partially make payments to current liabilities.

Boosting sales: The company may rely significantly on profitability and profit growth without incurring any additional operational expenses. Significant growth of this magnitude can be utilized to reduce debt and enhance the deficit proportion.

Stock that is being issued for the first time or that is being issued for the second time: The corporation might introduce additional or extra shares to increase its working capital. This money can be used to pay down outstanding loans while also lowering the overall debt. As a result of the debt decrease, the debt-to-asset ratio will be reduced.

Effective stock control: Storage can consume a significant portion of a company’s operating flow. Raising excessive amounts of inventory above what is required to satisfy customer requests on time is a loss of working capital. As part of the revenue transfer process, organizations can look at the ‘Days of Additional Inventory’ proportion to see how effectively inventory is maintained. Another approach that may be performed to minimize the debt to asset ratio is to improve inventory tracking.

Reducing your debt: If a corporation’s obligations have historically had extreme rates of interest, and the cost of borrowing is significantly lower, the firm may explore restructuring its previous debt. This would reduce all debt and leasing payments, allowing the corporation to increase its lowest part efficiency, cash resources, and reserve funds. This is a popular and simple method for negotiating fair arrangements for the company’s outflows and inflows.

Effective inventory management: Inventory may eat up a large percentage of a company’s current capital. Maintaining excessively high inventory levels above what is required to fulfill customer requests on time is a waste of cash flow. Organizations can look at the ‘Days of Inventory Holding’ ratio as part of the cash conversion process to assess how well inventory is handled. Another approach that may be performed to minimize the debt to total assets ratio is to improve inventory control.

Capital Structure ratio

Additional capital structure ratios that represent the weighting factors of the different funding sources in a firm, aside from the debt to asset ratio, are as described in the following:

- A debt-to-equity ratio means lenders have less security; a low current ratio means borrowers have a larger safety margin that is creditors believe the owner’s money can assist withstand any income and capital deficits. This metric shows how much debt money there is compared to how much money there is in the bank.

- The percentage of the proprietors’ investments made in the firm’s revenue fund is indicated by the percentage. Generally, it has been assumed that when a larger fraction of the proprietors’ capital is invested, the overall risk is reduced.

- The equity proportion, in contrast to the default rate, is frequently computed to emphasize the percentage of term deposits bearing assets to resources attributable to equity shareholders, that is equity funds or personal wealth.

Conclusion

The loan ratio is a useful measure of an organization’s ultimate viability. The company should keep a continual check on this proportion since lenders and potential investors will be looking at it. Investors are anxious about recouping their funds, and a larger debt-to-asset ratio raising worries about a company’s trustworthiness would result in less or no venture creation financing. As a result, the company should always strive to keep the proportion within an appropriate range.

FAQ’s

Why are debt levels essential in determining a company’s risk?

Debt usage proportions are important for analyzing a company’s risk since a rising debt load and interest commitments might jeopardize the company’s viability. The greater the proportion of capital borrowed funds, the larger the company’s possibility of loss.

What does a firm’s debt-to-asset proportion offer a guest?

The debt-to-total-assets analysis is used to calculate a firm’s capacity to generate funds through accumulated debt. The percentage is compared to other companies in the same sector to arrive at this conclusion. The greater a firm’s liabilities percentage is, the greater indebted it is.