In today’s borderless digital economy, businesses—especially those in high-risk industries—need reliable ways to process international payments. That’s where an offshore merchant account comes into play.

Whether you’re operating in e-commerce, travel, adult entertainment, or pharmaceuticals, setting up an offshore merchant account allows you to accept multi-currency payments, reduce chargebacks, safeguard against fraud, and expand globally—all while maintaining compliance and privacy.

But what exactly is an offshore merchant account? How do you qualify for one? What documents are required? And is it the right choice for your business?

In this article, we’ll walk you through everything you need to know about offshore merchant accounts—from setup to benefits, and why it’s a game-changer for businesses operating internationally.

What Is An Offshore Merchant Account?

Usually, e-commerce businesses placed in non-resident nations are the ones that go for an Offshore Merchant Account (OMA). It enables the business to accept payments via their website as well as other payment systems. Several internet-based firms, particularly the ones falling in the high-risk range, experience difficulties in obtaining merchant accounts, particularly from financial institutions as well as local account suppliers.

Domestic banks are typically conservative, requiring businesses to provide a variety of documentation as well as a history of credit purchases. As a result, the merchant account application process is time-taking and, in some instances, fruitless. Such digital marketers can open an OMA, offshore merchant account.

Domestic merchant account suppliers may not enable a significant number of transactions, thus merchants who want to steadily raise their revenue projections should use an OMA. This overseas merchant account will remain discreet in its dealings and will enable payments to be sent anywhere in the world.

These accounts also offer tax benefits because they are located in countries with no tax obligations. Adult amusement, Online drugstores, casino games, sportsbooks, electronic money, imitation goods, cigarette products, travel-based, and pharmaceuticals are positioned to gain the most from establishing an OMA, offshore merchant account.

How to Qualify For An Offshore Merchant Account?

Based on the nature of your offshore company, it might be critical to ensure that your already existing merchant account is an OMA. This section would be applicable, for instance, if your organization includes a digital commerce element or takes payments from any nation like the U.S.A, Germany, or Europe.

Nevertheless, not all sellers fall into such classifications as even small merchants may require such choices for their distinctive reasons, like receiving credit card payments from clients living overseas who require greater fraud safety measures than the ones currently provided by traditional local financial institutions.

Documents Required For Offshore Merchant Account

To continue with the process of forming an offshore merchant account, here are the papers that you would need:

- A canceled check

- An authorized, government-issued identification document, like a DL, driver’s license

- If relevant, 3 months of the latest transaction statements

- 3 months’ worth of financial records

- Chargebacks should be less than 2%.

- An SSN, Social Security Number, and/or an EIN, Employer Identification Number

A safe and fully functional site. In most circumstances, it is acceptable if the site has not yet been released as far as there’s a functioning website in a development platform.

We understand how tough it may be to locate the best OMA. If you’re someone who has run a high-risk company and attempted to get accepted for an overseas or foreign credit card transaction service, odds are you’ve been rejected in the first go.

We recognize what such risks entail for an organization. If it’s due to location issues or risk considerations like government limits on international currency payment processing, it doesn’t matter. Our staff has developed simple, convenient offshore merchant account services that are suited to each firm’s specific requirements. Our staff has developed simple, convenient offshore merchant account services that are suited to each firm’s specific requirements.

Applying For Your Offshore Merchant Account

There is no cost or obligation to apply for an overseas merchant account. However, you must register with the necessary paperwork. For an OMA, the minimum monthly transaction should be $50,000. Furthermore, a professional account manager will assist you throughout the application procedure. Your goal here would be to gain approval as soon as possible. And at a lower cost. Furthermore, it has a decent contract. Your request for an OMA will be approved within 6-8 working days. Furthermore, from this point, the entire registration file is obtained.

Offshore Credit Card Processing – Definition and Importance

A simple way to define an offshore credit card is by knowing that it’s a credit card that’s filed by an overseas financial institution that could be present anywhere in the world but nowhere in your residential country. Similarly, offshore credit card processing is a kind of merchant account service that’s provided by an overseas firm that lets the consumers take up services and then pay the amount using a credit card. This type of payment is safe and secure.

The role of an OMA is to take the transactions that your firm gets from abroad forward. It rapidly raises your business’s scope to grow with the addition of credit card processing. How? You can start taking payments from international ends safely. This also helps the customers by letting them pay you easily, and you can also accept the payment without facing obstacles.

But why is Offshore Credit Card Processing important? Here are some reasons why:

New technology

It is usually recommended that one should always embrace new technologies and learn to use them along with the present method to offer the best service using both, the old as well as the new payment method.

Seamless experience

The developers of this type of payment method are rigorously working to make things smooth for their users, and also are keeping up with the changing modes of transaction.

Ease of payment

Clients prefer to pay with credit cards, particularly in cafes, shops, and retail outlets that need network operators to accommodate a mode of payment for their consumers. Customers can also make purchases using their credit cards as well as other digital payment methods. Overseas credit card systems allowed merchants to take electronic payments in many currencies. Because of this payment mode, there is no bother of transaction discrepancies across international borders. It also takes credit cards that aren’t as prevalent or famous, which expands the company’s reach across international borders.

These services must be available online or over the phone for the companies’ or network operators’ consideration. It is also critical for the business to select a payment platform that offers secure transactions via secured portals and credit card handlers.

Multi-Currency Payment Processing with an Offshore Merchant Account

One of the key advantages of opening an offshore merchant account is the ability to accept multi-currency payments. This allows your business to process credit card transactions in a variety of international currencies—such as USD, EUR, GBP, CAD, AUD, and NZD—enhancing your ability to sell globally.

If your business serves international customers, enabling them to pay in their local currency improves trust and removes friction at checkout. With an offshore merchant account, you can streamline multi-currency billing under one robust payment gateway.

Key Benefits of Multi-Currency Payment Processing

1. Marketing Benefits

- Displaying prices in a customer’s local currency improves user experience and increases conversion rates.

- It builds credibility and reduces the chances of cart abandonment caused by unexpected currency conversion fees.

- You gain access to broader international markets, particularly English-speaking countries like the US, UK, Canada, Australia, and New Zealand.

2. Administrative Benefits

- Reduces chargebacks and customer disputes caused by currency discrepancies.

- Simplifies accounting and reconciliation by segmenting revenue streams by currency.

- Enables localized reporting, which supports better financial decision-making.

3. Commercial Benefits

- Offshore merchant accounts often offer competitive transaction fees for multi-currency processing.

- You can structure payments under a like-for-like currency setup, avoiding costly cross-border conversion charges.

- With proper planning, your business can achieve significant cost savings and tax efficiency through strategic use of offshore payment solutions.

Note: To maximize the benefits of an offshore merchant account with multi-currency support, work with a provider that offers dynamic currency conversion (DCC), flexible settlement options, and localized acquiring banks.

Terms & Conditions For Offshore Merchant Accounts

Charges for OMAs differ based on where the acquisition bank is situated. Most offshore banks provide competitive prices, especially to large volume, high-risk businesses. Settlement timeframes for overseas credit card transactions are determined by the number of transactions processed. Everyday settlements are available for large businesses, whereas small offshore commercial accounts may collect monthly or a few settlements each week.

The exchange rate varies from one country to the next. For instance, European exchange prices are cheaper than those in the United States, and charges in Europe are comparable with those in the United States.

The OMAs are known to save you cash on transactions when you got clients present in the same location as your acquiring bank. For example, when an OMA is in Europe, your Europe processing will be low in cost when compared to a transaction through a bank in the US.

The main point of consideration for an offshore transaction is card declines. Based on the financial institution, cards are seen as an aid to take forward cross-border processes. This can lead to an increase in card decline percentage. It all comes down to the laws of the nation where the acquiring bank is situated.

Advantages Of Offshore Merchant Account

Here are some of the advantages of opening an offshore merchant account:

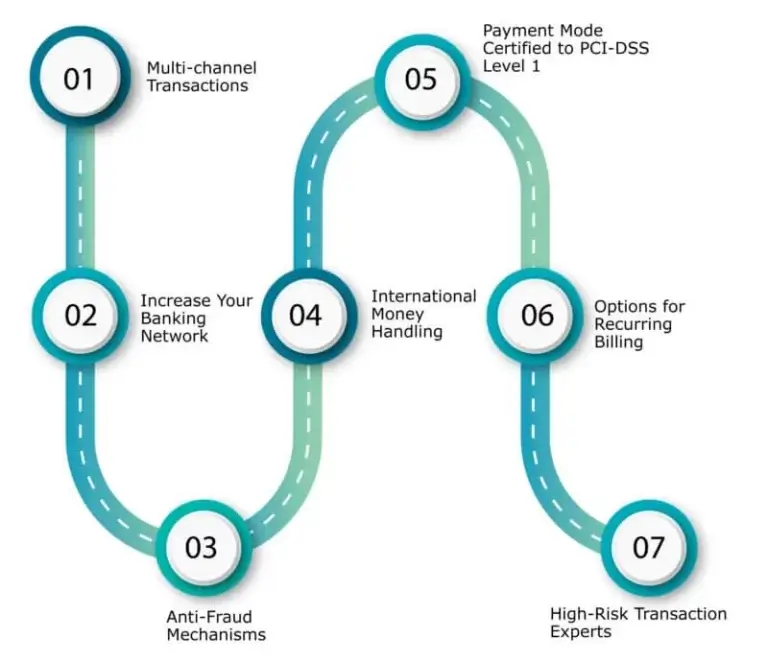

1. Multi-Channel Payment Support

Offshore merchant accounts allow you to accept payments through multiple channels, including websites, mobile apps, virtual terminals, and batch processing for bulk transactions. This flexibility enhances customer convenience and business efficiency.

2. Expanded Banking Network

By working with acquiring banks across various jurisdictions, you can diversify your banking relationships. This not only increases financial flexibility but also helps minimize disruptions due to regional banking restrictions or regulations.

3. Advanced Anti-Fraud Mechanisms

Many offshore processors offer customizable anti-fraud tools, including real-time transaction monitoring, geo-fencing, and rule-based filtering. These features help detect and prevent fraudulent activity, safeguarding your business and customers.

4. International Currency Support

Offshore accounts typically support over 50 currencies, allowing you to accept payments in multiple denominations. This is essential for global operations and can significantly improve your conversion rates from international customers.

5. PCI-DSS Level 1 Compliance

Most offshore merchant service providers adhere to the highest security standards, such as PCI-DSS Level 1 certification. This ensures your payment processing system is secure and compliant, protecting sensitive cardholder data.

6. Recurring Billing Options

Offshore accounts often come with flexible recurring billing solutions, making it easier to manage subscription-based services or memberships. This improves customer retention and automates revenue collection.

7. High-Risk Business Friendly

If your business falls under a high-risk category (e.g., adult entertainment, gaming, forex, or nutraceuticals), offshore merchant accounts are more likely to approve your application compared to domestic providers. These accounts are designed to support industries that face difficulties with traditional banks.

Conclusion

Setting up offshore merchant services gives high-risk business owners a secure means of accepting payments. Additionally, you might benefit from exclusive credit access to safeguard the company’s liquidity. Additionally, there are no volume restrictions on offshore merchant accounts.

If you want to have a seamless and easy process of opening an offshore merchant account, it is advisable to get in touch with our professional experts from OnDemand International, to understand more about the process of setting up an offshore account.

FAQ’s

What is an offshore merchant account?

An offshore merchant account is a type of bank account set up in a foreign jurisdiction that allows businesses to accept payments—especially credit card transactions—from global customers. These accounts are typically managed by acquiring banks or payment processors located outside the business’s country of incorporation.

Why would a business need an offshore merchant account?

Businesses often seek offshore merchant accounts to:

1. Access international markets

2. Accept payments in multiple currencies

3. Lower tax liabilities

4. Avoid high chargeback risks

5. Partner with acquiring banks in regions with fewer restrictions.

What are the advantages of offshore merchant accounts?

1. Multi-currency payment acceptance

2. Higher processing limits

3. Lower tax implications (in some jurisdictions)

4. Better fraud protection tools

5. Easier approval for high-risk industries

6. Expanded banking network

Is it legal to open an offshore merchant account?

Yes, opening an offshore merchant account is legal as long as your business operates within international regulations and maintains proper documentation and tax compliance.

What is offshore credit card processing?

Offshore credit card processing allows businesses to accept card payments through a foreign payment gateway or processor. It is ideal for companies that want to process high-volume international transactions securely and efficiently.