Revenue Recognition Services

Revenue recognition is an estimating regulation that estimates the specific situations under which profit is acknowledged. However, the ICAI issues AS 9 Revenue Recognition.

The Institute of Chartered Accountants of India ( ICAI ) illustrates revenue as the whole inflow of money or receivables, or any other interest, that occurs from the normal actions of an association, such as the sale of products and rendering of services.

The income should be calculated in terms of the price charged to clients for products and services. In the circumstance of corporation relations, income must be calculated by the commission amount.

However, it does not depend on the gross cash inflow, receivables, or any other consideration. The statement spoken above may contain exceptions where significant consideration is required.

- Construction contracts generate revenue.

- Revenue from government grants and similar subsidies

- Insurance companies generate revenue from insurance contracts.

Revenue recognition refers to the timing of revenue recognition in an organization’s statement of profit or loss. An agreement between the parties to a transaction determines the proportion of income that results from a transaction.

The amount of revenue is differentiated from the associated costs in the event of uncertainties. These uncertainties can have an impact on the timing of the revenue.

Application of AS 9 Revenue Recognition

This standard was originally issued by the ICAI in 1985. It was recommended for Level I groups, but it has been able to mandate all organizations starting from April 1, 1993. According to ICAI, the enterprise is a company as defined by section 3 of 2013’s Companies Act.

The term Level I enterprise refers to enterprises whose turnover in the preceding accounting year exceeded Rs. 50 crores. The turnover excludes any other revenue, as it’s only adequate for both possessing and subsidiary firms.

Brief on Revenue Recognition

- Revenue Recognition focuses on when revenue is recognized in an enterprise’s profit and loss statement.

- A treaty between the companies included in a transaction will usually determine the amount of revenue that results from the transaction.

- Uncertainties in the determination of the amount and any associated costs can have an impact on the timing of revenue.

The Key Elements of Revenue Recognition

These are the main elements of revenue recognition

- Sale of Goods

- Rendering of services

- Interest, Royalties, & dividends

- Sale of Goods

The sale of goods is a crucial element of the transaction’s revenue recognition. The dealer has lent the products to the buyer as consideration. The shifting of wealth in products is often due to the shifting of major dividends and dangers associated with the ownership.

There are circumstances in which the shifting or substantial dangers are not compatible with the shifting of products to the customer. These cases require that earnings be acknowledged at the period of product transfer to the customer.

Revenue must be recognized in these cases at the time the buyer transfers significant risks and rewards. This could include goods sent to the consignee under approval.

In many instances, the industry has cases where the performance is substantially complete before the execution of the revenue-generating transaction. In the following circumstances, the goods are valued at the net realizable price (NRV).

- If the sale is guaranteed by a Government guarantee

- Forward Contract

- There is little chance of failure to sell if there is a market.

These types of payments are not included in the significance of revenue, but they are occasionally identified in statements of gain and loss, such as farming yields or the mining of mineral ores.

- Rendering for Services

The performance of the service is also a key factor in revenue recognition for services. This can be further torn down into two categories:

- Proportionate Completion Method: This procedure of accounting dividends proportionately to the grade of fulfilment for each assistance in the gain and loss statement.

The ordinance of excess than one act is considered complete service. Each such act is considered complete, and the revenue is acknowledged.

- Completed Service Contract Method: This technique of accounting dividends when assistance is rendered under a treaty that has been finished or substantially finalized.

- Interest, royalties & dividends

They are usually utilized by the enterprise to give a boost to it.

- Interest:- After taking into consideration the outstanding amount as well as the applicable rate, interest is recorded on a time-proportion basis.

For example, if the Fixed Deposit interest is due on 30 June and 31 December, the revenue will be recognized as per the time proportion basis. The interest from January to March will still be received in June.

- Royalties:- This is the cost for use of trademarks, patents, and copyrights. Recognizing revenue must be done on an accrual basis following the agreement. Ex: If the supremacy depends on the number of books sold, it must be acknowledged only for that purpose.

- Dividends:- When the owner has the right to receive the income, the revenue must be acknowledged. It is natural when the firm announces bonuses on stocks and the directors agree to spend profits on its stakeholders.

Conditions for Revenue Recognition

The following conditions must be met to recognize revenue according to Indian Accounting Standards:

- The dealer must transfer the dangers and premia of ownership to the customer.

- The dealer no longer possesses control of the goods sold.

- Adequate actions will be impelled to collect payment for the goods and services.

- It is feasible to assess the revenue reasonably.

- It is feasible to assess the revenue costs reasonably.

- a) Performance refers to the Conditions set out in paragraphs (1) and (2). Performance is defined as when the seller does what is expected.

- b) Collectability is the condition mentioned in point 3. The seller must have reasonable expectations that he/she will be paid according to the performance.

- c) The above-mentioned conditions (4) and(5) are called Measurability. According to accounting guidelines, the seller must have the ability to match its expenses and revenues. Both earnings and expenditures should be assessed relatively.

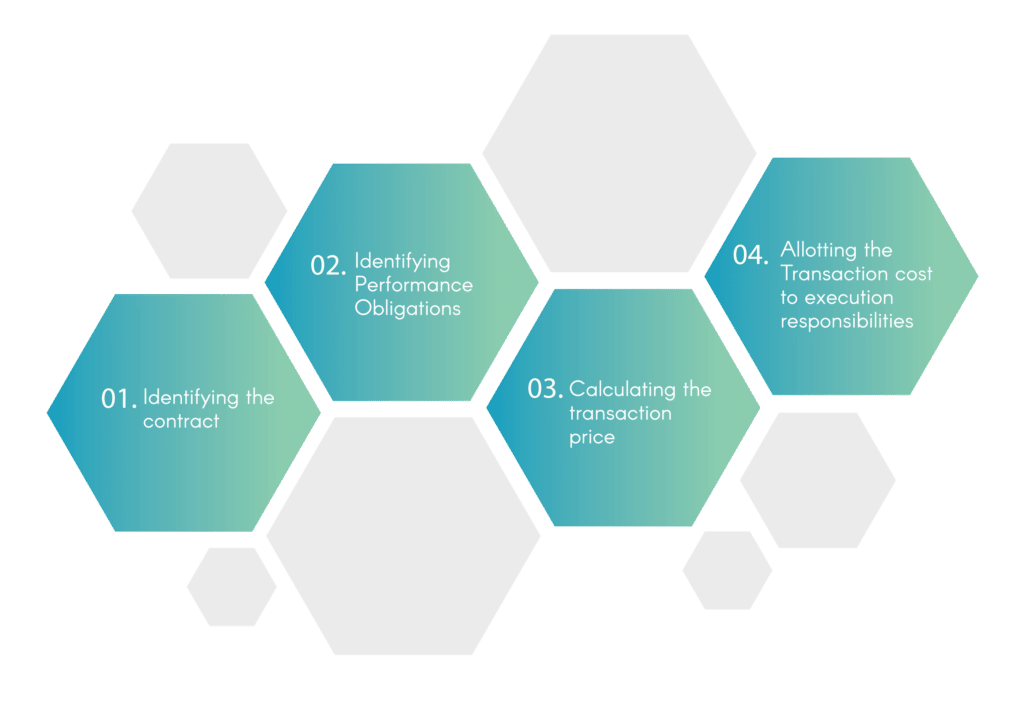

What are the steps to recognize revenue from contracts?

These are the five steps to revenue recognition in contracts:

Steps to Revenue Recolonization

- Identifying the contract

- Identifying Performance Obligations

- Calculating the transaction price

- Allocating the Transaction price to performance obligations

- Identifying the contract

- A contract must be signed if all conditions are met

- The contract must be approved by both parties (written, verbal, or implied)

- It is necessary to identify the point at which goods or services are transferred.

- It is important to identify the payment terms.

- The contract also contains commercial substances.

- There is a possibility of collecting payment.

- Identifying Performance Obligations

Sometimes, contracts include more than one performance obligation. A car sale that includes a complimentary driving lesson might be one example of two performance obligations. The first would be the car, and the second the driving lesson.

Each obligation must be performed separately. To be different from a product or service, the subsequent requirements should be fulfilled.

The products and assistance can be utilized by the buyer (or customer) on their own. The contract identifies the service or good.

- Calculating the transaction price

The price of the contract specifies the agreement cost. The price for a car is Rs. 6,00,000. This includes a complimentary driving lesson. This transaction would cost Rs. Only 6 lakhs.

- Allotting the Transaction cost to execution responsibilities

The selling prices of each execution must be used to determine the allocation price of the agreement cost to each execution obligation.

Uncertainties have an impact on revenue recognition

Below is a description of the impact of anticipations on revenue recognition.

- Revenue recognition expects that earnings be quantifiable. It is unfair to expect final collection at the period of the deal, or the rendering of assistance.

- Revenue recognition is delayed when the ability to assess the collection is not at a reasonable level.

- In certain litigations, revenue may just be recognized if it is relatively certain that the final gathering will occur. Revenue is recognized at the period of the deal, rendering of assistance, or instalments.

- It is recommended to adjust the revenue to reflect any uncertainty in Collectability that arises after the sale of a service.

- Revenue recognition is delayed if the consideration amount, an essential element, is not quantifiable within reasonable limits.

- Revenue of the period is properly recognized, even if revenue recognition is delayed due to uncertainty.

Checklist in Revenue Recognition Policy

Each Entity should assess while formulating a revenue recognition policy under Ind AS 115. This policy must be documented, reviewed, and approved by appropriate management levels.

It covers each performance obligation.

- Description of the Performance Obligation

- The shape of the agreement of bond for the accomplishment deficit.

- As the services are completed, the shifting takes place at one case in time: upon cargo or delivery.

- Transfer occurs over some time. This description includes the input method or methods used, as well as how they are applied.

- Qualitative economic information includes the customer’s type, geographical location, and the type and type of contract that has an impact on the nature, amount, and timing of revenues and cash flows.

- Important terms for expenses for feat obligations include when they are unpaid, what the relation is, whether it is cured or inconsistent and if the measure is inconsistent.

- This is the timing of performance obligations that refers to the usual timing of payments and the effect of these factors on contract asset or liability balances.

- Obligations to return or refund products and warranties, and the related obligations that relate to performance.

- Discuss the possibility that the company is acting as a principal or agent regarding the performance obligation. Also, discuss how the deficit was created.

Fundamental financial statement disclosures for Revenue Recognition

The preparation of financial statement disclosures will be made easier by having a revenue recognition policy. To recognize revenue, the companies must disclose the following information in their financial statements:

General Disclosures

- Transparency is required to allow financial statement users to see the revenue and cash flow from customers’ contracts.

- It is important to disclose the beginning and end values of contract assets and liabilities, as well as related receivables.

- It is essential to publicize the transition.

Disaggregated Revenue

The timing of the goods transfer and the effect of economic factors on each stream of disaggregated income must be considered when calculating the revenue.

Performance Obligations

- Transmitting the nature of the goods and services that the enterprise has promised (including when it will act as an agent).

- It is essential to publicize the specific terms of payment.

- All obligations to return, refund, or perform similar duties must be disclosed.

- It is also necessary to disclose the warranty types and related obligations.

Important Judgments

- All judgments that have a significant impact on the determination of the amount, as well as the timing of revenue from contracts customers with you and any modifications to them, must be judgmental.

- Disclosure of conclusions relating to the timing of fulfilment and the transaction cost and proportions allotted for execution.

- Provide information about the methods, inputs, and assumptions used to estimate a variable consideration estimation that is strained.

Conclusion

Revenue recognition refers to the timing of revenue recognition in an organization’s statement of profit or loss. An agreement between the parties to a transaction determines the proportion of earnings that results from a transaction.

As to manage revenues and maintain the transaction history throughout the business. That’s where Odint consultancy comes in, however, we will assist you and guide you during the entire process. Feel free to contact us, our highly, well-experienced EXPERT will help you out.

FAQ’s

What is the revenue recognition principle?

Accounting guidelines require that revenues are shown on income statements in the period they were earned and not the cash collected. This is a portion of the accrual footing.

How do you acknowledge revenue?

Revenue recognition involves five steps.

- Identify the contract you have with a customer.

- Identify the performance requirements in the contract.

- Calculate the transaction price.

- Assign the prices to performance obligations.

- Recognize revenue

What types of revenue recognition are there?

These are some of the revenue recognition techniques that you can use:

- Sales Basis Method.

- Percentage of completion method.

- Completed Contract Method

- Cost Recovery Method

- Installment

- Revised Revenue Recognition Method

How does collectability impact revenue recognition?

If the vendor determines that collectability is less probable than anticipated, the vendor will stop recognizing revenue. However, it won’t have to reverse any revenue previously recognized. The customer has fulfilled all payments promised to him and the vendor no longer has any obligations.

What is the significance of timing revenue recognition?

It is important to adhere to the revenue recognition standard because it allows you to see what your profit margin is in real-time. This is vital to ensure credibility in your finances. Financial reporting can help you keep your transactions in line