Annual Filing Requirements for Singapore Companies 2022

All Singapore enterprises must comply with specific legal requirements every year, regardless of their size or structure.

Comparatively to other countries the legal obligations in Singapore are fairly easy and simple. However, an entrepreneur who is busy might miss a deadline, which could lead to penalties and fines.

- ACRA is the Accounting and Corporate Regulatory Authority which acts as the central regulator of industries in Singapore.

- IRAS is the Inland Revenue Authority of Singapore which collects taxes & lays out the filing requirements for each year.

The following sections provide in-depth information on each of these conditions. If you’re looking to establish a new Singapore firm or prepare annual reports for your current company, make sure to read the entire article.

ACRA Annual Report (AR) Filing using ACRA

ACRA is a public body that monitors and enforces the rules of business in Singapore. Singapore Companies Act imposes all businesses to create an Annual Report to ACRA at least 30 days after hosting an AGM. An Annual Return must be documented with BizFile the online filing system.

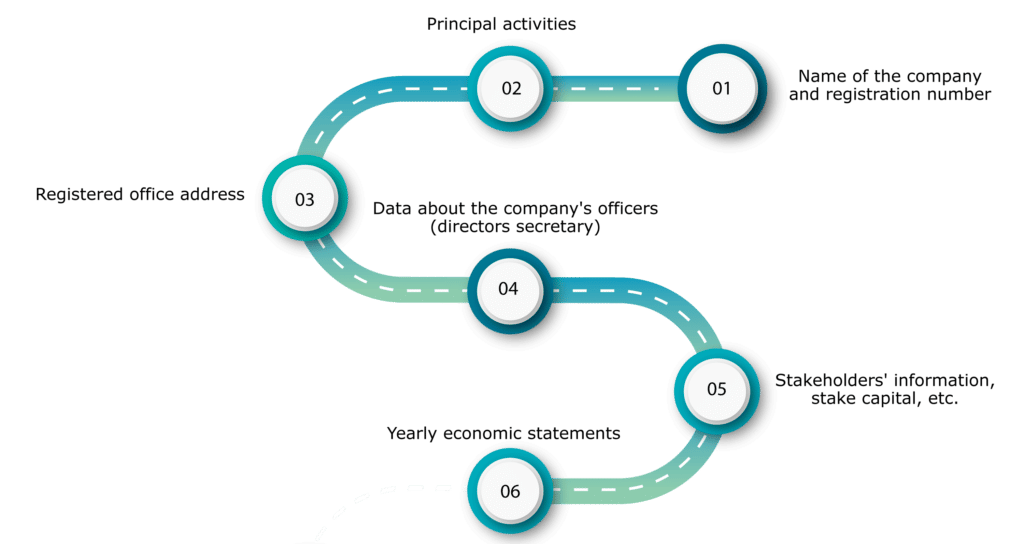

What exactly is an Annual Report?

The Annual Report is a series of documents that contain up-to-date details on:

- Name of the company and registration number

- Principal activities

- Registered office address

- Data about the company’s officers (directors secretary)

- Stakeholders’ information, stake capital, etc.

- Yearly economic statements

Exemption from Attaching Financial Statements

Certain businesses are exempt from having to include their financial statements in the Annual Report. These include:

- Small-sized companies: As a reminder, small businesses are those which fulfill 2 of the 3 criteria listed below:

- The entire annual revenues are less than

- Entire possession shouldn’t be higher than S$10 million.

- Maximum 50 employees

- Private companies exempt (EPC): An EPC is a business that has:

- There shouldn’t be higher than 20 stakeholders.

- There are no corporation shareholders (i.e. all shareholders are natural people)

- Dormant EPC: A dormant EPC is an entity that hasn’t operated any business or produced any revenue during the previous financial year.

Financial Statements in XBRL Format

Since 2014, every business needs to provide their financial statement using eXtensible Business Reporting Language (XBRL) to the Singapore government.

XBRL can be described as an XML format that is used to create financial documents that companies use to share financial information. The format is free and open-source to use.

Certain businesses are not required to prepare financial statements using XBRL for example:

- International companies as well as their affiliates

- Guaranteed companies

- Companies are permitted to have the right to make financial reports in conformity with accounting standards different in SFRS, SFRS for Small Entities, and IFRS

- Solvent Exempt Private Companies (EPC) EPC: An EPC is an entity that is:

- Not more than 20 shareholders

- There are no Corporate shareholders (ie all shareholders are natural people)

Annual Return Filing without Holding an AGM

In certain situations, ACRA enables firms to apply for annual tax returns without having an AGM. The company must submit its appeal via BizFile.

ACRA could still reject the application, particularly when a company has submitted it multiple times. In the event that an application has been approved, ACRA generally will notify the applicant within 14 days.

However, an organization that submits its annual tax return in late compliance with ACRA is obliged to pay a late fee. The late fee will increase in proportion to the amount of time in default rises.

Annual General Meeting (AGM)

The Singapore Companies Act requires companies to organize annual General Meetings (AGM) for their stockholders unless the company has decided to not organize AGMs through the passage of a shareholder resolution.

If the company does not wish to hold an AGM and all issues that must be resolved during the AGM are resolved through the passage in writing resolutions.

What exactly is an AGM?

AGM is a shareholder’s gathering that occurs every calendar year at a specific time. This annual meeting grants shareholders the opportunity to take part in the making of certain decisions by the business, and this requires their consent.

One of the main goals of an AGM is to look at the financial statements of the company and its shareholders. As per section 175, under the company, a firm & officials who fail to convene an AGM are subject to a fine that can be as high as S$5,000.

To avoid being prosecuted, ACRA enables firms & officials to spend an amount of $300 for makeup1 costs per violation.

Annual Financial Statements

In accordance with the Singapore Companies Act, all companies that are incorporated within Singapore as well as the entire Singapore subsidiaries of overseas corporations are required to create and submit financial statements that are in line with Singapore Financial Reporting Standards.

Singapore Financial Reporting Standards (SFRS) is in identifying which is founded on & substantially identical to International Financial Reporting Standards (IFRS) which are allocated through the International Accounting Standards Board (IASB).

The Key Facts

- Financial statements shouldn’t have been made more than 6 months into the progression of the AGM

- The director of the company must confirm the financial statements and be accountable for their accuracy and accuracy as well as preparation in conformity with Singapore accounting guidelines.

- Dormant and small-sized companies that meet certain standards can prepare financial statements that are not audited.

Financial Statements

The financial declarations that need to be established include the following:

- Directors’ Report and Statement of Directors

- Independent Auditor’s Report (if applicable)

- The Statement of Comprehensive Earnings (Gain & expense statement)

- Statement of Financial Situation (Balance sheet)

- Money Flow Statement

- Statement of Equity of Shareholders

- The Corresponding Notes for Financial Statements

Audit Exemption

To make it easier for the filing procedure, Singapore frees specific firms from amassing their financial statements examined, this includes:

- Small-sized companies: A small company is any firm that meets two of the following 3 criteria:

- The entire yearly revenue should be lesser than S$10 million

- Total possession shouldn’t be higher than S$10 million.

- Maximum of 50 workers

- Dormant firms: A dormant company is any business that has not been operating a business and has not earned any income during the last tax year.

These companies may prepare audited financial statements.

Yearly Tax Returns Filing using IRAS

IRAS (Inland Revenue Authority for Singapore) is Singapore’s government agency that collects taxes in Singapore. All Singapore businesses are required to submit annual tax returns through IRAS.

Tax returns for the year include two tax returns:

- Estimated Chargeable Income, which must be noted within 3 months from the time of fiscal year-end

- Tax return for corporate income that must be completed by November 30th for filing on paper or before the 15th of December for online filing.

Filing Estimated Chargeable Income (ECI)

ECI represents an estimation of the company’s tax-deductible earnings for the current fiscal year that was completed.

IRAS requires that companies submit ECI within 3 months following the close of the financial year. The company will be notified by IRAS to submit ECI in the final calendar month for the year.

In July 2017, the following companies aren’t required to submit an ECI:

- Companies that have less than S$ 5 million in annual revenue

- Companies with ECI are NIL

Making a Corporate Income Tax Return

Alongside filing ECI and ECI-S, businesses must also submit the annual tax returns with C-S or form C, but at a later time. There are currently two deadlines for filing the corporate income tax return that uses IRAS

- November 30th for filing paper

- December 15th is the deadline to file electronically

The dates for filing a corporation’s returns for income taxes are those of the fiscal year following the year that ended with the financial year’s end. In the example above, If the fiscal period ended in March 2017 the corporate income tax return has to be submitted by November 30, or the 15th of December in the year 2018.

Companies who file using the form C must also contain Annual statements, and tax estimations including detailed profit and loss statements, as well as other documents supporting them.

A C-S form is a simplified form of the tax return for corporations that do not require businesses to submit tax computations as well as financial statements. For filing C-S, businesses must satisfy the required requirements listed below:

- The company needs to be incorporated in Singapore

- The business must not earn at least $5 million of revenue per year.

- The company isn’t claiming one of these:

- The carry-forward of capital allowances/losses

- Group relief

- Investment allowance

- Tax credit for foreign tax and tax deductions at the source

Tax File for Dormant Companies

In general, dormant businesses must still submit a tax return for their corporate clients in conjunction with IRAS however, IRAS permits some exceptions. Dormant companies may apply for the waiver of tax returns if they satisfy the following requirements:

- The company has not carried out business, nor earned any money.

- The firm has filed either its Form C-S or Form C, accounting statements & tax estimations as of the time of ceasing the company

- The company cannot hold any investment (e.g. shares, real properties, fixed deposits). If the company has assets, it is not allowed to earn any money from the investments (real properties, shares, fixed deposits).

- The company has to be removed from registration for goods and services tax (GST) for tax advantages.

- The business must not be planning to restart the company in the upcoming 2 years.

- IRAS typically can process the waiver in two months.

Failure to comply with IRAS

ECI Non-Compliance

- Failure to file the ECI within 3 months of the close of its fiscal year

- Failure to meet the requirements to be exempt from submitting ECI

If a business lags to meet ECI obligations, IRAS will mail the firm a Notice of Assessment (NOA) which gives an estimate of the firm’s earnings.

To avoid penalties for late payments or other enforcement actions the company must transfer the estimate of earnings to IRAS within one month, regardless of whether the company doesn’t agree with IRAS estimates.

If the business does not accept IRAS the assessment, it may issue a Notice of Opposition. The notice of opposition should contain the reasons to file ECI late (or failing to file ECI or file ECI, as the situation could be) as well as the latest estimated ECI.

When making a Notice of Opposition that the business is legally required to pay taxes for the ECI within one month.

Corporate Income Tax Non-Compliance

- Inability to classify a corporation income tax return

- Failure to submit an application form C or C-S before the due date

In the majority of instances, businesses can avoid penalties simply by filing a tax return for income. In the event of not filing, corporate taxes can result in four phases, with each stage resulting in escalating penalties.

Phase I: IRAS can dispense a general notice of assessment (NOA). Once the NOA is issued the business is required to make payment of the tax estimate in the NOA within one month. In addition to the tax estimate, the company must also pay its income tax.

The company is able to submit a Notice of Opinion to IRAS in the event that it believes IRAS’s assessment was not accurate. After you have paid for the estimate and submitted its income tax returns the tax obligations of the company are completed for the year.

Phase 2. IRAS issues an Outstanding Tax Refund Notice and assesses the composition fee up to $1000. The company should submit an income tax return, and also pay the fee for composition. The company is able to appeal to have the fee removed, however, the majority of fees are not ruled out.

Phase 3. IRAS is expected to issue a Notification of the provisions of Section 65B(3) from the Income Tax Act to the director, along with a composition charge that can be as high as $1000. To prevent further liabilities, the official has to submit all the documentation decreed by the notice of Section 65B(3). Section 65B(3) as well as pay the composition fee within 21 days.

Phase 4. IRAS issues the official Summons to emerge before a judge. To prevent from taking off to court, the official needs to present the report offered within the Summons & pay the summons costs at least a week prior to the court date.

If the director fails to produce the documents required and pays the summons charge and is not able to pay the summons fee, she will be asked to appear before a judge. In court, the director could be penalized up to S$1,000 and the company will be required to submit an income tax return.

Phase 5. Failure to submit for more than 2 consecutive years. If a company hasn’t filed its tax return for income after 2 years, it may be subject to the following penalties:

- A penalty equal to twice the tax amount

- A fine up to $1,000.

Streamlining the filing of the Annual Tax Returns

The filing annually in Singapore requires the preparation of financial statements, coordinating and holding annual general assemblies, and submitting the appropriate returns within the timeframes allowed for each ACRA along with IRAS.

Inability to satisfy all of the regulations can result in serious penalties for a business. That’s why the majority of firms in Singapore prefer to use a professional company service supplier that can provide expert assistance throughout the annual filing process. They can also make sure that the business is compliant with Singapore laws.

Certificate of Compliance and Compliance Rating

A business that has met the annual filing requirements will receive an ACRA green checkmark in its online directory for the name of the company. The company then qualifies to be awarded a Certificate of Compliance.

If a business fails to adhere to these guidelines then the company is issued the red cross mark and cannot be eligible for the certificate. It is crucial for entrepreneurs to adhere to the annual filing requirements.

Anyone who wants to work with a company will be able to view the basic details of the business and the score it has earned on ACRA’s web-based directory.

Conclusion

Every Singapore corporation that is incorporated must make sure of the timely filing of tax returns and forms to ACRA as well as IRAS. A reliable corporate services company can assist in ensuring that the requirements of compliance for the company are met, and its business is shielded from legal pitfalls.

If you still have any queries related to the annual filing requirements for Singapore companies, we are ODINT Consultancy, here to help you out in each & every step of yours.

FAQ’s

Which businesses are required to prepare a return for the year?

All businesses, I.e. PLC, Solo Proprietary, limited liability company, section 8 company, etc. must make an annual tax return using the MCA each year. Alongside filing an MCA annual returns, businesses must report a tax return for income.

Must a business submit an annual tax return each year?

An annual statement of the corporation must be filed each year up until a date that is not later than the annual return date (ARD).

What is the deadline for a business to file an annual report?

Private companies are required to complete their annual tax return within seven months of the end of the financial year. The filing of your annual return in time will provide timely and correct disclosure to all stakeholders.

What happens if a business isn’t able to file its annual return?

Penalties for failing to file a company’s annual report (Form MGT-7 as well as Form AOC-4) are scheduled to be raised to the amount of Rs. 200 per day.

What’s the deadline for annual filing as per company law?

All firm is expected to report the annual records & annual profit gain as per The Companies Act, 2013 within 30 days & 60 days respectively from the verdict of the AGM.