When starting a business, you must consider whether an LLC or a sole proprietorship is the right business form for you and your needs. These two corporate structures can drastically affect how you handle your organization from a legal, tax, and management viewpoint.

In this article, you will learn what sole proprietorships and LLCs do, as well as how to pick the appropriate one for your business purposes. Read the complete article to know more about LLC vs Sole Proprietorship.

In a Nutshell: LLC vs Sole Proprietorship

The most common company types of business structures are limited liability corporations (LLCs) and sole proprietorships. Forming a sole proprietorship is the least difficult and requires less documentation. An LLC entails initial paperwork and expenses, but it could offer your company long-term benefits that are worth the expenditure. When deciding between a sole proprietorship and an LLC, two important considerations to take into account are legal protection and potential tax benefits.

What is a Sole Proprietorship?

A sole proprietorship is a form of corporation owned by the person who operates it. It serves as the automatic selection for individuals running businesses who have not established an alternative formal business arrangement, such as an LLC. Within a sole proprietorship, the distinction between personal and business assets and expenses is non-existent. The individual takes full personal accountability for all of the company’s obligations and duties.

Only one individual can form a sole proprietorship. Your unincorporated business will change into a general partnership if you bring on a partner.

People who operate on a contract basis frequently elect to file their taxes as sole proprietors, including independent contractors, consultants, and personal trainers. If you’re just starting or aren’t yet earning enough money to cover the fees of an LLC, this is the simplest route to go. Nonetheless, depending on the nature of your firm, a sole proprietorship may be the best option even if you’ve been in operation for years. Everything will rely on your revenue, the kind of your firm, and your particular management preferences.

Merits of Sole Proprietorship

- Quick Dissolution: If you wish to close or dissolve the business, the process is often less difficult and easier than winding up other business forms.

- Low Initial Investment: Starting a sole proprietorship often needs less initial investment than other business types. Individuals with modest financial means may benefit from this.

- Tax Advantages: Individual tax rates are applied to sole proprietors rather than corporation tax rates, which might result in possible tax savings. Furthermore, you can frequently deduct company costs from your taxed income.

- Total Control: You have full authority over all corporate decisions and activities. Before making choices, you do not need to discuss them with partners or shareholders.

Demerits of Sole Proprietorship

- Unlimited Liability: Being individually liable for the debts and obligations of a sole proprietorship is one of its major disadvantages. This implies that if the company runs into financial difficulties or is sued, the owner’s assets are in danger. Creditors have the right to seize the owner’s personal property, savings, and other support to fulfill the business’s liabilities.

- Potential for Growth Is Limited: Sole proprietorships may struggle to expand due to limited resources and the owner’s competence to undertake all activities. The owner’s capacity to manage rising workloads and expectations may limit growth.

- Credibility Issues: Some clients, suppliers, and partners may regard sole proprietorships as less reputable than more significant, more established business organizations such as corporations or limited liability companies (LLCs). This perception may affect the company’s ability to acquire high-value clients or obtain favorable arrangements.

- Minimal Capital and Resources: When compared to bigger business forms, sole proprietorships may have restricted access to finance. Raising capital can be difficult because the owner’s savings and credit are often the primary sources of funding. This might limit the company’s potential for expansion.

What is a Limited Liability Company (LLC)?

An LLC (Limited Liability Company) is a corporate structure that blends the characteristics of both a corporation and a partnership or sole proprietorship. This structure grants its owners, referred to as members, a level of protection known as limited liability. Essentially, this means that the personal assets of the members are typically safeguarded from the company’s debts and legal obligations.

A legal document must be filed with your state to establish an LLC as a business entity. One owner (referred to as a “member”) or several owners may constitute an LLC.

Once established, an LLC has a distinct legal identity from you, the owner. As a result, if your firm is sued or fails to pay its obligations, a business creditor cannot lawfully pursue your assets. The bankruptcy of an LLC is additionally seen as distinct from the owner’s. An LLC can also assist in protecting you from accountability for the activities of your workers if you have any.

A single-member LLC is initially taxed in the same manner as a sole proprietorship, but it has the option to elect to be taxed as either a C corporation or an S corporation. Because of their tax flexibility, LLC owners can select the tax structure that will cost them the least money for their particular company. The possibility of corporation taxes is a key factor in some organizations’ decision to create an LLC.

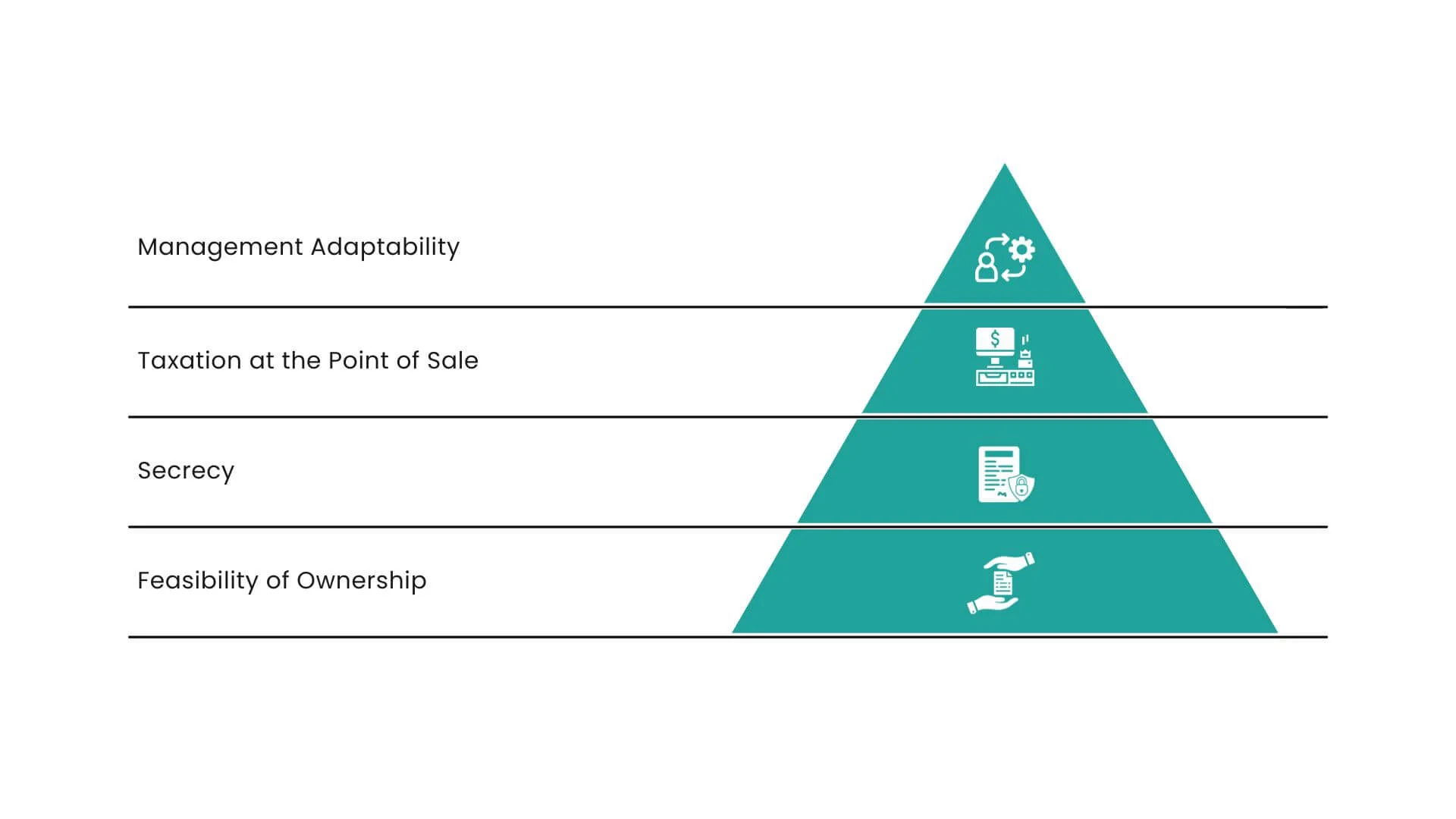

Merits of Limited Liability Company (LLC)

- Management Adaptability: In terms of managerial structure, LLCs provide flexibility. Members can administer the firm themselves or choose managers to handle day-to-day operations. This adaptability allows for a configuration that best meets the owners’ abilities and preferences.

- Taxation at the point of sale: Income earned by an LLC is not subject to entity-level taxation. It is instead passed through to the owners and taxed on their tax filings. This may lead to tax savings for businesses.

- Secrecy: An LLC’s owners have the option of keeping their personal information private. Corporations, alternatively, are compelled to keep public records.

- Feasibility of ownership: An LLC’s ownership can be easily transferred. This could be advantageous for companies that are expanding or seeking new investors.

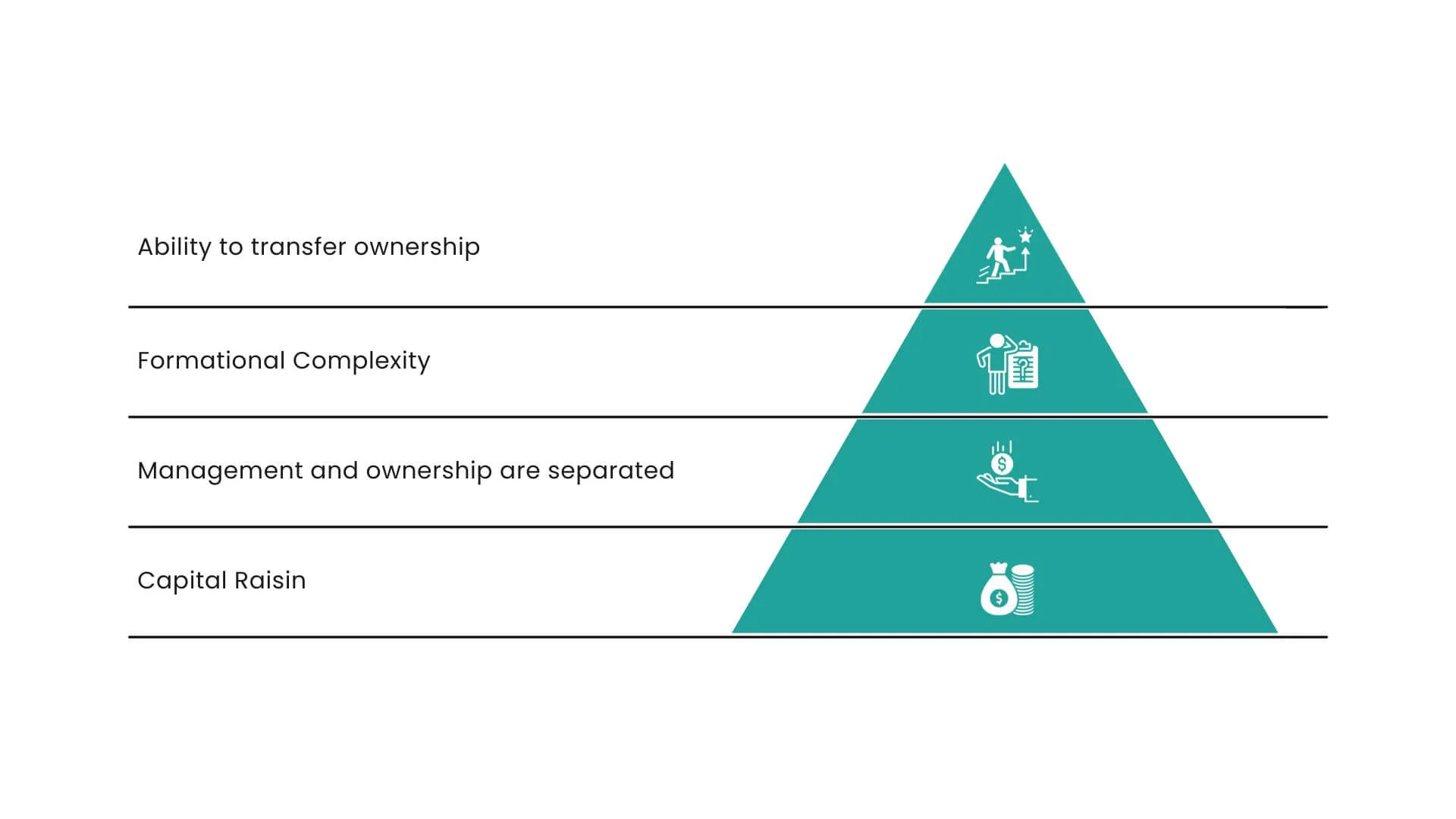

Demerits of Limited Liability Company (LLC)

- Ability to transfer ownership: It could be more challenging to transfer ownership of an LLC than of a corporation. This is because all LLC members must agree to the transfer, and the LLC’s operating agreement may contain specific conditions for transferring ownership.

- Formational Complexity: An LLC has more paperwork and administrative obligations than a single proprietorship or partnership. You’ll need to submit articles of incorporation, draft an operating agreement, and maybe adhere to state-specific restrictions.

- Management and ownership are separated: There may be a separation of ownership and management within an LLC. This can lead to conflicts if managers are not also members or if members are not actively involved in the day-to-day operations.

- Capital Raising: When it comes to generating funds through the sale of stock or recruiting investors, LLCs may encounter more obstacles than corporations since ownership interests in an LLC are not as easily transferable as shares in a corporation.

Operating Your Business as an LLC vs Sole Proprietorship

Operating a business as a sole proprietorship means there is no legal separation between you and your company as the sole owner. You are not required to keep your personal and company credit cards and bank accounts separate. When it comes time to pay your taxes, it will be simpler to track down business costs if you create a separate checking account for your company.

With an LLC, it’s critical to keep your business and personal money fully separate. You’ll require a business bank account, as well as the ability to sign documents and contracts on behalf of the firm rather than yourself. Keeping things separate protects your liabilities by demonstrating that the LLC has its own distinct identity.

An LLC provides more tax choices than a sole proprietorship. All independent entrepreneurs work for themselves. Your company revenue and costs will be shown on Schedule C of your tax return, and you will pay personal income tax on your earnings. Single-member LLC owners are automatically categorized as self-employed sole proprietors for tax purposes, which means they are responsible for paying their own Social Security and Medicare taxes, commonly referred to as “self-employment taxes.” However, an LLC might decide to be taxed like a corporation. With corporation taxation, an LLC owner might be a firm employee rather than self-employed. Some company owners discover that taxing as an S corp saves them money on self-employment taxes and allows them to save more for retirement. If your solo firm is beginning to turn a profit, consult with an expert accountant about the optimal tax position for your organization.

Forming an LLC over a Sole Proprietorship

There are some of the reasons for considering opening an LLC over a Sole proprietorship are mentioned below:

- Your assets should be shielded from any financial and legal liabilities.

- You desire to benefit from any applicable local, state, or federal tax advantages associated with establishing an LLC.

- In the future, If you wish to add more owners to the business, which is simple with an LLC.

Costs of Formation and Registration: LLC vs. Sole Proprietorship

The setting up method and expenses will be strongly determined by your state, whether you choose a sole proprietorship or an LLC. At OnDemand International, our experts provide a more in-depth look at what to expect on the LLC side. Many of the providers in our finest LLC services directory can assist you in locating organizations that make the registration procedure quick and uncomplicated regardless of what you want.

Conclusion

Creating an LLC can help you prepare yourself for development while also protecting you from responsibility. People also consider forming an LLC when their company reaches a specific income level and the additional expenses and procedures make sense from a tax perspective. This varies by state and business kind, so consult with OnDemand International’s specialist for your business and financial-related queries and compare the taxes you’ll pay with each business form.

FAQ’s

When incorporating an LLC, you will incur some expenditures. The first step is to pay a one-time formation fee, which can range from $50 to several hundred dollars depending on your jurisdiction. You may choose to engage a lawyer or an online LLC filing service to draft and file the papers on your behalf. The cost for this service can vary, and it is not part of the state filing fee. Moreover, if you opt for a registered agent company to act as your registered agent, you will incur an annual fee ranging from $50 to $300 for their services.

Certainly, you can transform a sole proprietorship into an LLC by submitting an LLC application to the appropriate state authority, which may be the Secretary of State, Business Bureau, or Business Agency in your state.

Many considerations will come into play, including the level of personal accountability you’re ready to accept, how you want to be taxed, and how much paperwork and costs you can bear.