Are you about to be transferred to the Netherlands (NL) due to work reasons and to contribute to their economy? Are you looking to save some taxes? If yes then keep on reading. Here, we’ll discuss the benefits of the Netherlands 30% Ruling, which will help you save some taxes. In brief, Expats can benefit from the Netherlands 30% ruling as it acts as a relief for the employees who are transferred from abroad to work in the Netherlands. This system might seem a bit more complicated, but once an individual understands it, they can easily reap benefits from it.

So if you’re curious about just how Dutch 30% ruling will help you live a hassle-free life in the Netherlands– keep reading, because, in this article, we’ll understand about the 30% ruling of Netherlands, how it works, what its benefits are, and how one can apply for it.

What is Netherlands 30% Ruling?

Netherlands 30% Ruling is a Dutch income tax facility, which permits an immigrant to collect 30% of their salary tax-free. This tax advantage usually targets highly skilled employees who have been hired from abroad to work in the Netherlands for a specific employment role.

In the greater depth, any immigrant transferred to the Netherlands for work purposes will be subject to Dutch income tax, plus they’ll be confronted with extra costs (housing costs, relocation cost, etc) known as extraterritorial costs. So in order to help the expats, Netherlands’ tax authorities came up with a tax break, namely the Dutch 30% Ruling, which provided much-needed relief to the Expats.

As per Dutch law, an employer can reimburse employees for extraterritorial costs by providing a tax-free allowance which comprises 30% of the salary, by jointly (employer and the employee) submitting an application with the Dutch Tax Authorities who will then check about the eligibility. Although not every expat in the Netherlands is eligible for it, there is a long list of conditions that need to be fulfilled by an employee. This is a way to attract skilled employees from abroad to provide useful resources and use their expertise for their growth. The 30% ruling will remain valid for a maximum of 5 years, it used to be 8 years prior to 2019.

The responsibility of collecting taxes, custom duties, and excise duty lies upon Belastingdienst. The Dutch tax office (Belastingdienst) is a government organization that is responsible for imposing and collecting taxes on the behalf of their state.

How does the Netherlands 30% ruling work?

Generally, the salary agreed by employee and employer would be split into two parts, one will be the base salary while the other part will be the 30% ruling allowance which will be exempt from taxation.

Although, the 30% ruling holder should know that the pension and employee insurance schemes are based on the remuneration package after the split for the 30%-allowance. As the contributions to the pension and insurance schemes are levied on the taxable salary which will eventually result in lower future benefits. There is a possibility to add a 30% allowance on the basis of pensionable salary (building upon higher salary), with the help of a labor costs scheme which has been introduced as a mandatory scheme. An individual will have specifically mentioned that the 30% allowance can be part of the pensionable wage.

How long Netherlands 30% ruling stay valid?

Previously, the maximum applicable period for Dutch 30% ruling was 8 years. But as of 1st January 2019, the Dutch Government has reduced the maximum applicable period to only 5 years. This doesn’t sound like good news considering it’s a long time, but compared to 8 years, 5 years seems reasonable.

Who can claim the Netherlands 30% ruling?

- The employee must work with an employer who is registered with the Dutch tax office and pay Dutch payroll tax.

- The employee has specific expertise to offer, which will be determined based on a salary norm, which gets updated annually. (These norms does not apply to employees who are working in the Netherlands in the area of education)

- For 2021, the threshold for an employee’s taxable annual salary must be €38,961 or more, while the threshold for an employee with a master’s degree up to the age of 30 taxable annual salary must be €29,616 or more.

- Prior to employment in the Netherlands, the employee needs to make sure that since the last 18 out of 24 months, they were not residing within 150 km from the Dutch Border.

- Both parties (employee and employer) have to agree in writing through the application of a 30% ruling.

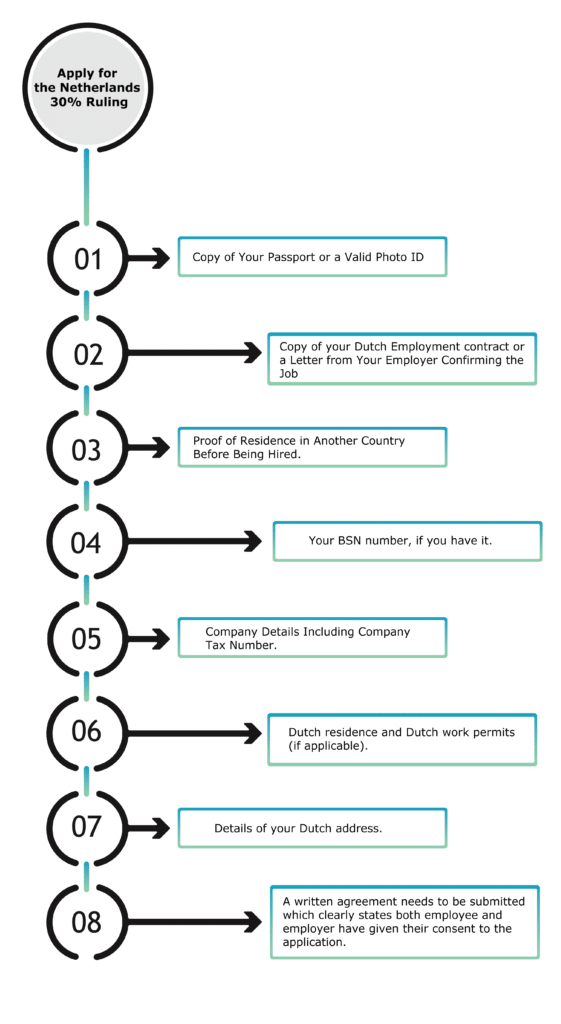

How to apply for the Netherlands 30% ruling?

To be eligible for the 30% ruling employer and employee have to jointly submit the application, within 4 months after getting employed in the Netherlands, and that application must be filed to the tax office. But even if you are late (not within 4 months) for it, you can still apply although the facility will be effective from the first day of the month preceding the month in which your application was successful.

The documents that you’ll need to provide to the Dutch tax office are:

- Copy of your passport or a valid photo ID.

- Copy of your Dutch employment contract or a letter from your employer confirming the job.

- Proof of residence in another country before being hired.

- Your BSN number, if you have it.

- Company details including company tax number.

- Dutch residence and Dutch work permits (if applicable).

- Details of your Dutch address.

- A written agreement needs to be submitted which clearly states both employee and employer have given their consent to the application.

Benefits of the 30% ruling in the Netherlands?

Apart from tax-free salary, 30% Ruling has many other benefits such as:

Partial non-resident status

The 30% ruling allows the expat to opt to be taxed as a deemed non-resident taxpayer. A partial non-resident holder won’t have to report their income from savings and investments, although they have to report that income if it comes from Dutch real estate or shareholding in a Dutch BV. In general terms, an Individual will be regarded as a non-resident taxpayer in “box 2” and “box 3”, while for “box 1” you’ll still be taxed as a resident taxpayer. So apart from real estate and shareholding in a Dutch BV, you won’t have to pay tax on any other investments.

Driver’s license

Expats to whom 30% ruling applies, can also obtain a Dutch license by exchanging it with their foreign driver’s license. Mostly to obtain a Dutch driver’s license one has to appear for the driver’s license test once again, but with the 30% ruling an individual can obtain the Dutch driver’s license without any driving test. Even the holder’s family members can enjoy that benefit, if they are registered at the same address as the holder of the 30% ruling.

Read More: Dutch Income Tax Calculator

Conclusion

In case the tax authorities won’t grant you the status of the 30%-ruling, still, an individual can reimburse their expenses tax-free, provided that expenses qualify as extraterritorial expenses. The most important step, to make sure that you are able to reimburse the expenses is the submission of receipts and invoices to the employer, as there should be proof that those expenses were actually incurred by the expat. If you want to make sure that your extraterritorial expenses are reimbursed, feel free to seek out professional help. We will provide you with all the necessary information that you’ll need and cater to your requirements with a solution that will serve your interest.

FAQ’s

How much time does it take to register an Indian company?

If under any circumstances the 30% ruling holder has to switch between jobs, they’ll have to discuss with their employer and then proceed to apply for the ruling once again for the remaining duration. if the employee meets the salary criteria and the period doesn’t exceed more than 3 months between the end of employment with the old employer and the starting of the employment contract with the new employer.

What to look in an employment agreement?

Your employment contract should clearly and separately mention the Netherlands 30% ruling if you are eligible for it, the agreement should be drafted in such a way that 30% tax-free allowance will be shown separately (as an addition to the base salary).

Can I apply for the 30% ruling even after 4 months?

Yes, one can apply for the 30% Ruling even after 4 months of starting employment activities as there’s no particular rule stating that there are any restrictions regarding the same. Once applied, the ruling will be effective from the first day of the month preceding the month in which your application was successful.