Earnings per share is the amount paid to shareholders for each share they own. This is a key component of financial metrics used in business. Investors typically use this to calculate the worth of a company’s shares and compare it to the market price.

Earnings per share show the company’s profitability status. The higher the earnings per share, the greater the profitability of the firm. This also draws numerous fresh and beneficial investments to the organization. It is one of the most effective indicators for determining the financial soundness and stock value of a firm.

Are you a business owner looking to set up and grow your business internationally? At OnDemand International, we make the registration process straightforward, guiding you through each step to establish your business in your target market seamlessly.

What is Earnings Per Share (EPS)?

Earnings Per Share (EPS) is a financial ratio that measures the portion of a company’s net profit attributable to each outstanding share of common stock over a specific period. It is calculated by dividing the company’s net income (after deducting preferred dividends) by the number of outstanding shares.

While the EPS figure for a single company provides insight into its profitability, it becomes significantly more meaningful when compared to other companies within the same industry or evaluated alongside the company’s share price.

For example, if two companies operate in the same sector and have a similar number of outstanding shares, the one with a higher EPS is generally considered more profitable. Moreover, EPS is often used in conjunction with the Price-to-Earnings (P/E) ratio to assess whether a stock is undervalued or overvalued. A lower P/E ratio suggests the stock may be undervalued, while a higher ratio could indicate an overvalued stock.

Why Is EPS Important?

EPS is one of the most popular profitability metrics in fundamental research. Here’s why it matters:

- Investor Decision-Making: A higher EPS suggests a more profitable company, making its stock more attractive to investors.

- Valuation Tool: EPS is used to calculate critical ratios such as the Price-to-Earnings (P/E) ratio, which compares a firm’s stock price to its earnings.

- Performance Tracker: EPS trends over time can help investors determine if a company is expanding, stagnating, or declining.

- Comparison Across Companies: It enables comparison of profitability across companies, especially in the same industry.

Basic EPS vs Diluted EPS vs Adjusted EPS

There’s no one-size-fits-all formula for EPS. based on the level of complexity or the financial report being analyzed, you may come across three types:

| Type | Formula | Use Case |

| Basic EPS | (Net Income – Preferred Dividends) / Outstanding Shares | Standard measure, used in most financial statements |

| Diluted EPS | Adjusted Net Income / Fully Diluted Shares (includes convertible securities) | More conservative, accounts for dilution from options, etc. |

| Adjusted EPS | Adjusted Earnings (excludes one-off items) / Shares | Focuses on core operational profitability |

These formulas help investors view profitability from different angles — from core business performance to worst-case dilution scenarios.

Earnings Per Share Formulas

The most commonly used EPS calculation is:

EPS = (Net Income – Preferred Dividends) / Weighted Average Outstanding Shares

Breaking Down the Components:

Net Income

Net income is a business’s net profit after accounting for expenses, taxes, interest, and depreciation. It appears on the income statement and serves as the starting point for calculating EPS.

Preferred Dividends

Preferred dividends are distributions made to preferred shareholders. Because these are not available to ordinary shareholders, they are deducted from net income in the EPS formula.

Weighted Average Outstanding Shares

Rather than using the number of shares at year-end, the weighted average over the reporting period gives a more accurate picture — especially if the company issued or bought back shares during the year.

Diluted EPS Formula

Some corporations issue convertible instruments, such as stock options, warrants, or convertible debt, which can be converted into shares in the future. These can dilute existing shareholders’ earnings.

Diluted EPS = (Net Income – Preferred Dividends) / (Outstanding Shares + Convertible Securities)

Adjusted EPS Formula

Adjusted EPS excludes non-core, one-off, or irregular items such as:

- Asset write-downs

- Restructuring charges

- Gains from discontinued operations

Adjusted EPS = (Net Income – One-Time Expenses + One-Time Gains) / Shares

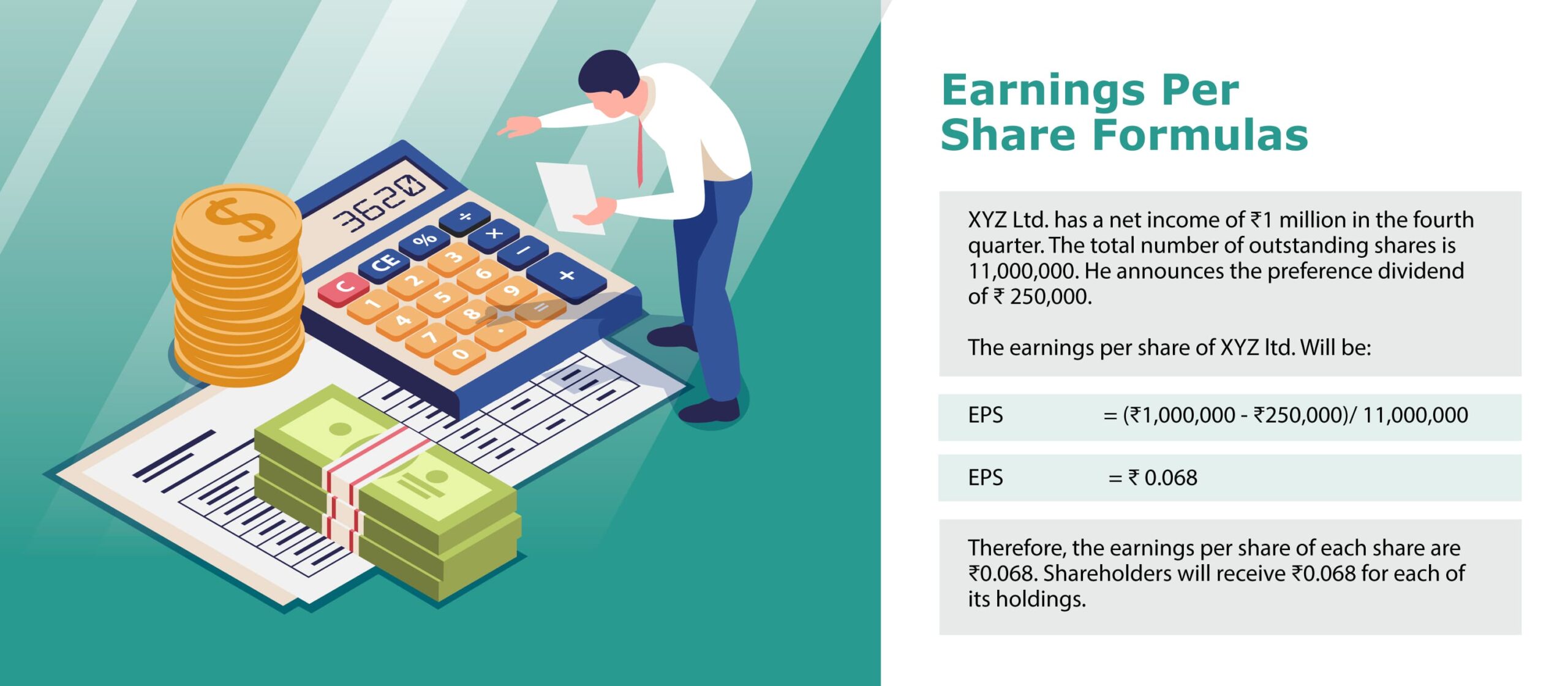

Example of Earnings Per Share Formula

XYZ Ltd. has a net income of ₹1 million in the fourth quarter. The total number of outstanding shares is 11,000,000. He announces the preference dividend of ₹ 250,000.

The earnings per share of XYZ ltd. Will be:

EPS= (₹1,000,000 – ₹250,000)/ 11,000,000

EPS= ₹ 0.068

Therefore, the earnings per share of each share are ₹0.068. Shareholders will receive ₹0.068 for each of its holdings.

Read Difference: Difference Between Bookkeeping and Accounting

How EPS is Used in Financial Analysis?

EPS is a key component in evaluating both absolute profitability and relative valuation.

Here’s how it fits into broader financial analysis:

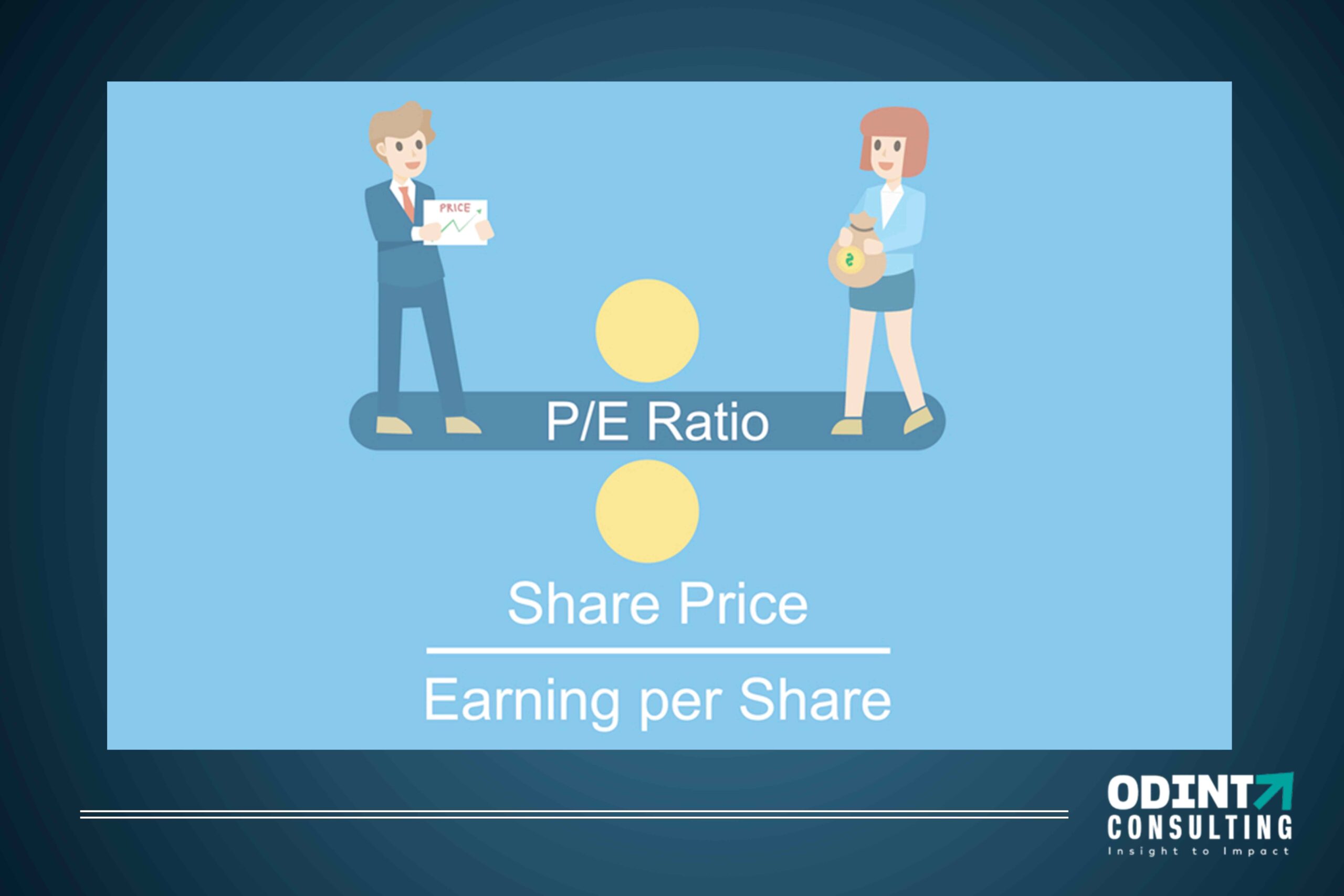

1. Price-to-Earnings (P/E) Ratio

- P/E Ratio = Share Price / EPS

- A low P/E may indicate undervaluation, whereas a high P/E shows that investors anticipate future growth.

2. Return on Equity (ROE)

- Determines how effectively a corporation leverages shareholder equity to generate profits.

- EPS is part of the numerator in the calculation.

3. EPS Growth Over Time

Investors look at the EPS growth rate year over year to assess performance consistency.

4. Dividend Payout Analysis

Companies with stable or growing EPS are better positioned to pay dividends.

Conclusion

The Earnings Per Share (EPS) formula is more than just a calculation — it’s a vital indicator of a company’s profitability, performance, and investment potential. Whether you’re a retail investor evaluating stocks or a founder preparing financial reports, understanding EPS empowers you to make informed, data-driven decisions.

From basic EPS to diluted and adjusted EPS, this metric offers a clear lens into how well a company is generating returns for its shareholders. When paired with tools like the Price-to-Earnings (P/E) ratio and Return on Equity (ROE), EPS becomes a cornerstone in assessing stock value, business growth, and market confidence.

FAQ’s

What affects earnings per share?

Many internal shares impact the earnings per share. But some of them directly impact profits, preference dividends, outstanding shares. These are buyback of shares, splits, mergers, restructuring, acquisitions, and accounting policies.

How earnings per share can be manipulated?

Earnings per share can be manipulated either by adjusting the net income of the company or by adjusting the total number of outstanding shares of the company.

What do negative earnings per share mean?

Negative earnings per share mean that the company is spending more than it has earned. That simply means the company is losing money. Negative earnings per share do not necessarily mean that stock must be sold.

How many types of earnings per share are there?

There are mainly five types of earnings per share. These are reported earnings per share, GAAP earnings per share, ongoing earnings per share, pro forma earnings per share, and retained earnings per share.

Why is earnings per share important?

Earnings per share are one of the most significant factors which help in determining the share price of the company. Higher earnings per share mean higher profits of the company, and it has more profits for distributing to shareholders.