If you are a business owner earning income through a Singapore-incorporated company, avoiding taxation on the same income in two countries is a critical tax consideration.

Whether your income is taxed once or twice depends primarily on the tax residency status of your company and whether your home country has a Singapore DTA (Double Taxation Avoidance Agreement) in place. Singapore has signed DTAs with most major economies, allowing businesses and individuals to legally avoid double taxation.

This article explains what the Singapore DTA means, how Singapore’s tax treaties work, eligibility and process to claim DTA benefits, and types of income covered.

What is Double Taxation?

Double taxation occurs when the same income is taxed in two different countries. This typically happens if you:

- Earn business profits from trade between two countries

- Are employed in a country other than your country of residence

- Earn foreign income such as dividends, interest, or royalties

In such cases, both countries may claim taxing rights, resulting in the same income being taxed twice.

Why Do Countries Enter Into Double Taxation Avoidance Agreements?

Countries enter into DTAs to promote cross-border trade and investment while ensuring fairness in taxation. DTAs help by:

- Preventing double taxation on the same income

- Reducing uncertainty in international tax planning

- Clearly defining taxing rights between countries

- Encouraging foreign investment and innovation

- Improving cooperation between tax authorities

What is Singapore DTA?

Singapore DTA refers to the Double Taxation Avoidance Agreements signed between Singapore and its treaty partner countries.

Key points:

- Singapore DTAs apply to tax residents of Singapore and the treaty country

- Only income taxes are covered (not customs duties or indirect taxes)

- DTAs define Permanent Establishment (PE) to determine taxing rights

Permanent Establishment Under Singapore DTAs

A Permanent Establishment may include:

- An office, branch, or place of management

- Workshops, warehouses, farms, plantations

- Construction or project sites

- A dependent agent who:

- Regularly concludes contracts

- Maintains inventory for delivery

- Procures goods exclusively for the business

Eligibility for Availing Tax Relief Via Singapore DTAs

Nevertheless, Singapore’s tax treaties are fair and reciprocative. With most countries, you must satisfy the following conditions to be able to avail the benefits of a DTA:

- You’re a professional, specialist, or other individual earning income that arises in Singapore and tax resident in Singapore (present in Singapore or gainfully employed in Singapore.

- You’re a business whose effective place of ‘management and control’ is located within Singapore.

How to Claim the DTA Relief?

- You would need to file a Certificate of Residence if you are an individual earning income from a foreign country in that country.

- You would need to file a Certificate of Residence from Non-Residents to Inland Revenue Authority of Singapore (IRAS)

Incomes covered under Singapore DTAs

Singapore DTAs cover the following incomes

- Income from immovable property

- Business profits

- Shipping and air transport

- Associated enterprises

- Dividends

- Interest

- Royalties and fees for technical services

- Capital gains

- Artistes and sports-persons

- Salary and pension from government service

- Non-governmental pensions and annuities

- Students and trainees

- Teachers and researchers

- Income of government

- Other income

Methods of Relieving Double Taxation in Singapore

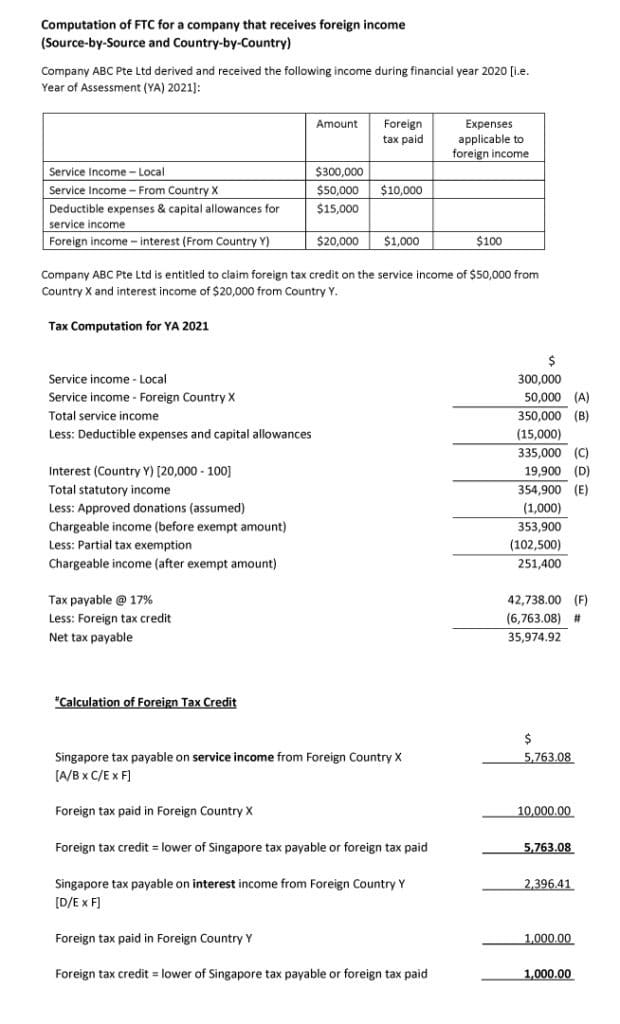

1. Tax Credit

A tax credit will be provided for the exotic tax suffered by a taxpayer for any holder’s trained tax committed on the related earnings. The percentage of tax value of owner’s assistance is generally prohibited to the worst of the paid/payable in the different house states.

Tax credit solace is normally pertained to as Double Tax Relief (“DTR”) in Singapore. The lawsuit for DTR should be earned while filing annual revenue tax returns (Form C) and should be exhibited in the corporation’s tax estimation for any holder.

2. Tax Exemption

- The increased corporate fee ratio (headline fee ratio) of the exotic country from which the dividend was earned is at least 15% for any individual.

- The foreign revenue had been subjected to price in the different nations from which they were obtained. The price at which the unfamiliar payment was taxed can be varied from the caption rate for payers.

Tax deductions for any Individual – Section 13(7A) of the Singapore Income Tax Act

Tariff rates for citizens and individuals in Singapore, all uncommon revenue amassed in Singapore will be protected from tax if the Comptroller is comfortable that the tax privilege is useful to the selves.

3. Tax Sparing Credit

Under a DTA, tax credit is generally accessible in the nation of housing only if the earnings have been taxed in the nation of base. Tax sparing prestige is a particular aspect of credit whereby the country of housing concedes to give a credit of the tax which would have been spent in the country of source but was not, i.e., “spared”, under different laws in that nation to facilitate financial improvement.

The tax limiting credit prerequisite is usually found in DTAs between a country which requests tax reasons to persuade foreign investment and a developing country which is money exporting. The value is given by the capital-exporting nation under its ordinances to stimulate investments.

4. Diminished Tax Rate

Under this aspect of relief, income is taxed at a lower rate and is favorable to the following grades of income: interest, earnings, and revenues from global shipping and by air carriers.

5. Relaxation by Deduction

Here, household tax is correlated on the distant earnings after subtracting foreign tax withstood. Singapore does not enable a deduction of foreign income tax. However Singapore reduces your tax outgo. Thereafter, it taxes the percentage of foreign income you earn (i.e. net of foreign tax) in the Singapore region.

6. Unilateral Tax Credit

If you are a Singapore tax citizen obtaining the next foreign revenue from nations which Singapore has yet to assume an Escape of Double Taxation Agreement (DTA), you can get a unilateral tax credit for the foreign prices paid on such income under Section 50A of the Singapore Income Tax Act.

Income originated from any experienced, consultancy and other employment provided in any province outside Singapore;

Dividends; or Profits arisen by an overseas branch of a Singapore resident company.

Singapore gives you a tax credit under Section 50A if you earn foreign sourced royalty from a non-treaty country, provided the royalty is not:

acquired rapidly and indirectly by an individual citizen in Singapore or a permanent organization in Singapore; or is deductible against any Singapore-originated earnings.

Example of Double Taxation Relief Calculation

Tax Reliefs on Types of Income with Reference to India

1. Business Profits

As per the DTA, the benefits of an enterprise are available just in the state where the business activities are done. If a Singapore-based business has a long-lasting establishment in another country, the benefits owing to the super durable establishment will be taxed uniquely in the other country.

2. Interest, Royalty, and Dividend

The DATA indicates the rates appropriate on account of pay from interest, sovereignties, profit, and dividends, the tax rates in the DATA are lower than the predominant tax rates in the nations that are gatherings to the understanding.

3. Interest

Without the settlement, the retention tax rate in Singapore for any interest paid to non-occupants is 15% while in India the rate goes from 5 – 20% (contingent upon the sort of interest) in addition to overcharge and cess. Under the DTA the tax on interest is as per the following:

- 10% of the gross sum, in case of interest, is paid on the loan which is conceded by a bank continuing financial business or any such monetary organization.

- 15% of the gross sum in any remaining cases.

4. Royalty

Without the settlement, the retention tax rate in Singapore for any sovereignties paid to non-inhabitants is 10% while in India the retention tax rate for any royalty paid to non-occupants is 10% in addition to overcharge and cess. Under the DTA, the tax rate for sovereignties is 10-15% relying upon the sort of royalty paid to non-occupants.

5. Dividends

Preceding April 1, 2020, India didn’t demand any retention tax for dividends. Nonetheless, the organization delivering dividends bears a profit dissemination tax (DDT) of 15% (in addition to overcharge and cess) while delivering the profit to its shareholders. The beneficiary investor is absolved from delivering any tax on profit. Hence, in India, the shareholders today deliver no tax on dividends except for when the organization settles a tax.

From April 1, 2020, India has nullified the DDT and the dividends will be taxed in the beneficiary’s hands. All things considered, India has presented a profit retaining tax. The rate will be 10% for dividends paid to shareholders in India and 20% whenever paid to unfamiliar financial backers (the India-Singapore DTA decreases this rate to 10 or 15% as portrayed beneath).

Read more : Dividend Declarations Explained

In Singapore, profit circulations by an organization are sans tax. Furthermore, the beneficiary investor is likewise excluded from tax on profit pay.

The India-Singapore DTA states that profit pay is taxed in the beneficiary’s condition of the home as follows:

- 10% if the beneficiary organization holds at least 25% of the portions of the organization delivering profit and

- 15% in any remaining cases.

The presentation of the new profit tax system by India sets out exceptional freedom for generous tax reserve funds by making a Singapore organization an investor of an Indian organization. This can be exceptionally useful to both unfamiliar and Indian shareholders. For addition to this, see our blog entry Singapore benefits from India’s new profit tax strategy.

6. Capital Gains

Article 13 of The DTA constrains the nation in which capital gains are responsible for tax payments. Another significant aspect of the India-Singapore DTA is the regulation of the advantages of sentences that were submitted in the policy signed between the governments in 2005.

7. Limitation of Benefits Clause

In 2005, the India-Singapore DTA was changed. The change gives that any capital acquired that emerges on the offer of property or offers are taxable just in the nation where the investors reside. This amendment proves useful to Singapore since the nation doesn’t require any tax on capital increases. For example, if a resident of Singapore sells portions of an Indian organization, it will be excluded from capital increases tax both in India and Singapore. This is an exceptionally huge tax advantage of the DATA that is intended to support interest in India from Singapore registered businesses and organizations.

However, to keep away from the abuse of this exception particularly by third-country inhabitants who set up holding organizations in Singapore to profit from the capital additions exclusion, the arrangement added a “Limit of Benefits (LOB)” provision. Under this provision, a Singapore incorporated organization won’t be qualified for the exclusion from capital increases if the sole motivation behind the foundation of the organization was to profit from this advantage. Furthermore, organizations that have insignificant business tasks in Singapore, with no congruence in business exercises won’t be qualified for this advantage. Because of the LOB provision, the arrangement isn’t material to shell organizations.1.

Singapore’s Tax Treaty Network

All the existing terms inferred by Singapore since 1965 to duration are categorised as mentioned:

- Detailed – These consensuses normally encompass all varieties of dividend.

- Limited – These authorizations enclose only payment from ferrying and/or other carriers.

- Treaties which have been guaranteed but not ratified – These are either extensive authorizations or restricted unions which do not have the terms turned into law yet.

Conclusion

Understanding the Singapore DTA (Double Taxation Avoidance Agreement) is essential for businesses and individuals earning cross-border income involving Singapore. With one of the world’s most extensive tax treaty networks, Singapore offers a highly efficient and transparent framework to prevent double taxation on income such as business profits, dividends, interest, royalties, and capital gains.

By correctly establishing tax residency, maintaining commercial substance, and claiming relief through the appropriate mechanisms—such as tax credits, exemptions, reduced withholding rates, or unilateral tax relief—taxpayers can significantly reduce their overall tax burden while remaining fully compliant with international tax laws.

Whether you are structuring investments, expanding globally, or earning foreign-sourced income, leveraging the Singapore DTA network allows you to optimise tax efficiency, improve cash flow, and enhance long-term business competitiveness.

FAQs

What is Singapore DTA?

Singapore DTA refers to the Double Taxation Avoidance Agreements signed between Singapore and other countries to prevent the same income from being taxed twice. These treaties allocate taxing rights between countries and provide tax relief mechanisms.

Who can claim benefits under the Singapore DTA?

Singapore DTA benefits can be claimed by Singapore tax residents and tax residents of treaty partner countries, provided they meet residency and substance requirements.

Does Singapore have a DTA with India?

Yes. Singapore and India have a comprehensive Double Taxation Avoidance Agreement covering income such as business profits, dividends, interest, royalties, and capital gains, subject to Limitation of Benefits (LOB) provisions.

What types of income are covered under Singapore DTAs?

Singapore DTAs generally cover:

1. Business profits

2. Dividends

3. Interest

4. Royalties and technical service fees

5. Capital gains

6. Shipping and air transport income

7. Pensions and employment income

How do I claim Singapore DTA benefits?

To claim Singapore DTA relief:

1. Obtain a Certificate of Residence (COR) from your tax authority

2. Submit the COR to IRAS or the foreign tax authority, as applicable

3. Claim relief while filing your annual tax return

Does Singapore tax dividends under DTA?

No. Dividends received in Singapore are tax-exempt. However, withholding tax may apply in the source country, often reduced under applicable DTAs.