Introduction

Are you planning to expand your business in Asia and looking for the best destination? Company registration in India is one of the most strategic decisions entrepreneurs can make due to the country’s massive market of over 1.4 billion people.

Registering a company in India gives investors access to one of the world’s fastest-growing economies, a rapidly digitizing society, and a consistently strong inflow of FDI—even during global downturns.

This updated guide covers the complete process for Indian company registration, including requirements, benefits, business structures, taxation, and regulatory compliance.

What is Indian Company Registration?

Indian company registration refers to the legal process of incorporating a business under the Ministry of Corporate Affairs (MCA), enabling the company to receive its Certificate of Incorporation, CIN, PAN, TAN, and legally operate in India.

Why Choose India for Business Setup?

India has emerged as one of the most attractive global markets due to its workforce, digital transformation, and political stability. Below are the major reasons businesses prefer company registration in India:

Key Reasons to Choose India

- 3rd Most Attractive FDI Destination Globally

- 1.4 million+ Active Companies

- 32 Global Unicorns Registered in India (each valued at USD 1B+)

- 419.5 Million Consumers by 2030

- High Digital Competitiveness

- Continuous Business Reforms (Ease of Doing Business)

- Skilled workforce across tech, handlooms, manufacturing, and services

- Stable political and economic environment

How to Register a Company in India?

In order to open a business in India, you must follow the steps given below:

1. Check Company Name on MCA Portal

Visit the MCA website → MCA Services → Company Services → Check Company Name.

Ensure the name is unique and not similar to existing trademarks.

2. Obtain Digital Signature Certificate (DSC)

Document signing on the MCA portal requires a DSC for all directors and subscribers of the MoA.

3. Apply for Director Identification Number (DIN)

At least one director must have a valid DIN number to proceed with Indian company registration.

4. Create an MCA Portal Account

Directors must register on the MCA portal before filing the SPICe+ INC-32 form.

5. File e-MoA & e-AoA Using SPICe+

Submit the e-Memorandum of Association and e-Articles of Association.

6. Upload Documentation & Pay Fees

Submit all e-forms digitally and complete the payment.

7. Receive Certificate of Incorporation (COI)

After verification, the Registrar issues the COI, enabling you to legally operate.

8. Obtain CIN, PAN, and TAN

These identifiers are automatically issued during incorporation.

9. Post-Incorporation Requirements

Companies limited by shares must file a declaration of subscription and verify the registered office address within 182 days.

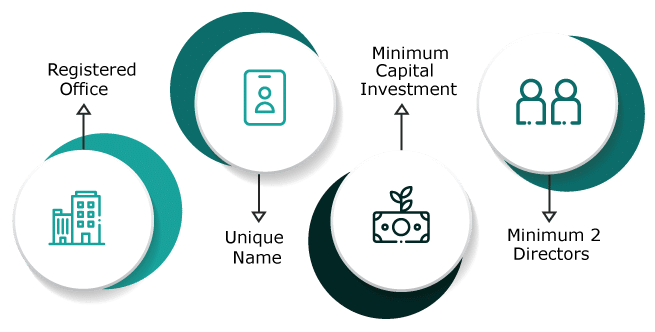

Checklist to Register a Company in India

Registered Office

It is not necessary to own a property for company registration in India. A rented place can also serve as your registered office address. But you do need to acquire an NOC (No Objection) from the owner of your rental to register successfully.

Company Name

The company’s name should not match already registered companies and trademarks.

Minimum Capital investment

The minimum capital requirement for a Pvt Ltd corporation is not specified.

Two Directors

A maximum of 15 and a minimum of 2 Directors are a must for an Indian Private Limited company registration. Also, one of the directors must be an Indian resident.

From the Directors or shareholders

- PAN Card or Passport copy – from any of the directors or shareholders

- ID Proof – any one of driving license, Voter ID, Passport, Aadhaar card

- Address Proof – any one of your Mobile bills, electricity bills, or latest bank details, or an NOC from your landlord if your office is a rental property.

- If your office is your own, get a copy of your sale deed/property deed

- Passport size photograph

For registered office address:

- NOC from the owner of the property

- Address Proof – Anything from Mobile bill, electricity bill, or latest bank details

You would require a scanned copy of all the listed documents above. Also, for address registration, it is not necessary to own your own company office.

Also Read: Best Current Bank Account for Small Business in India

Business Structures Available to Register a Company in India

In general, a foreign business can begin operations in India with the following types of organizational structure: Form an Indian Company:

- Through a Joint Venture

- Through a wholly-owned Indian subsidiary

You can do either of these through private or public limited companies.

The following types of companies can be incorporated in India:

One Person Company (OPC, for Indian Residents only)

This option lets you limit your liability, in case the business winds up, to business assets only. A single person can start an OPC with minimum documentation requirements. There is also no need to conduct annual general meetings or file returns with the Registrar of Companies.

Private Limited Company

A private limited company may be a company limited by shares in capital or by an amount that each company member promises to contribute to the assets of the company. Shares or contributions need to be mentioned in the Memorandum of Association of the company. You also need to have a minimum of 2 members and 2 directors, one of whom (directors) must be an Indian resident.

Public Limited Company

A Public Limited Company allows you to obtain funding via shares from the public. You need to have a minimum of 7 members and 3 directors, one of whom must be a resident Indian.

You can choose the type of company that best suits your needs and register the organization under the Indian Companies Act 2013.

4. Limited Liability Partnership (LLP )

A Limited Liability Partnership is a hybrid business structure where partners have limited personal liability for the firm’s obligations.

Key Features:

- Minimum 2 partners and 2 designated partners

- At least one designated partner must be an Indian resident

- Combines partnership flexibility with corporate limited liability

- Lower compliance than a private limited company

5. Other Options

- Partnership Firm

- Hindu Undivided Family (HUF)

Who Regulates Company Registration in India?

The Ministry of Corporate Affairs offers a wholly online process to help you register your business in India. However, documentation requirements can be complex. Your decision at this stage will also affect how much tax and what kinds of filings and audits you will need to legally perform each year.

Apart from registering your company in India, you also have the option of setting up:

Liaison Office

To collect information, promote imports and exports, or facilitate technical or financial collaboration.

Branch Office

To provide professional or consultancy services, perform research, develop IT products and services for the parent company, act as a buying/selling agent, etc.

Limited Liability Partnership (LLP)

This company form is relatively simpler to set up than a full-fledged company, requiring at least 2 partners and 2 designated partners, one of whom must be a resident Indian. However, your liability is limited by the number of shares in the LLP in India you own.

How to Decide Which Business Structure Type is Best for You?

Before registering your company in India, it is you must choose a suitable business structure that will fulfil all your requirements.

Here, are a few things that you need to consider while deciding on your business structure type.

1. Number of Owners

If you want to start a business single-handedly then you can go for a sole proprietorship or a One-Person Company (Indian residence mandatory). If more than one person is present, you should opt for a Limited Liability Partnership firm, a Private Limited Company, etc.

2. Level of risk

A One-Person Company and a Sole Proprietorship come with full risk assumptions by the founder, whereas in a company, there is no personal risk. In a partnership, the risk gets divided among the partners depending upon the mutual agreement.

3. Registration and maintenance cost

In the case of a proprietorship, registration and maintenance are inexpensive and one-time costs. However, companies have a high maintenance cost and need compliance requirements from time to time.

4. Credibility

Companies are more credible in terms of registration and other similar procedures but their financial records are accessible to the public. In a sole proprietorship, maintaining a reputation is the sole responsibility of the owner.

5. Tax structures

Different entities have different tax slabs.

Benefits of Registering Your Company in India

- Registration helps in generating more capital through reliable sources (banks & institutional lenders)

- The company becomes a separate entity and if anyone sues the company you will not be affected directly.

- Your liability towards the company is limited to the number of shares you own

- Your ownership and liabilities can be transferred from yourself to another person.

- You enjoy tax benefits for Directors and other employees

- Hiring professional management and ownership helps the company maximize its potential

- It becomes easier to build a brand reputation and attract genuine leads

- Scalability and expansion become easier

- Improved relationships with vendors, suppliers, industry associations, and customers

- Distinct corporate identity and existence

- Ensures perpetuity and continuity

- A company becomes more transparent and trustworthy in the eyes of the government.

Taxation for Companies in India

For the purposes of tax, companies are classified into domestic and foreign companies. While the former are liable to pay taxes on income they earn anywhere, the latter are liable to pay taxes only on income earned in India.

Income earned by a company incorporated and registered in India is further categorized as:

- Profits from the business

- Capital Gains

- Income earned from renting assets

- Income from sources such as dividends, interest, and so on

Tax rates on companies as well as individuals keep changing every year and are announced in the Annual National Budget declaration in Parliament. For the Financial Year that ended on March 31, 2021, the rates were as follows.

Domestic Company Tax Rates

| Company Type | Tax Rate | Surcharge (₹1Cr–10Cr) | Surcharge (10Cr+) |

| Section 115BA | 25% | 7% | 12% |

| Section 115BAA | 22% | 10% | 10% |

| Section 115BAB | 15% | 10% | 10% |

| Other Domestic Companies | 30% | 7% | 12% |

Foreign Company Tax Rates

- 50% for royalty/technical services (pre-1976 agreements)

- 40% for other income

GST in India

It is mandatory for companies manufacturing or supplying goods and services in the Indian market to register for the Goods & Services Tax (GST). This includes foreign companies without a place of business in the country.

The GST replaces the previous system of Value Added Taxes (VAT), Excise taxes, service taxes, etc.

The GST is made up of 3 components- CGST, SGST and IGST.

- The Central GST (CGST) is levied on sales where goods/services are transferred within state borders.

- The State GST (SGST) is levied on sales where goods/services are transferred within state borders.

- The IGST is levied on the inter-state sale of goods or services.

Who should register for GST?

- Previously registered taxpayers of Value Added Taxes (VAT), Excise taxes, service taxes, etc.

- Taxpayers without a place of residence in the place where he/she supply goods and services

- Any taxpayer in India whose annual turnover is INR 40,00,000 (INR 1000,000 in the North Eastern and hill states of India) or above needs to register for the GST

- Input service distributors and agents of suppliers

- Those to whom the Reverse Charge Mechanism of the GST is applicable

- E-commerce aggregators and their suppliers

- Businesses supplying information or database services from outside India to a person residing in India.

The GST requires taxpayers to register on the GSTIN website, file monthly and annual returns, file to receive Input Tax Credit, e-way bills for goods being transported, and so on.

Also Read: Sell Products Online Without GST Number

Conclusion

Registering a company in India opens the door to one of the world’s fastest-growing economies, offering businesses unmatched access to a 1.4-billion-customer market, rapid digital adoption, and strong government support for entrepreneurship.

With multiple business structures, favourable tax regimes, and a robust legal framework, Indian company registration empowers both local and foreign investors to build scalable, credible, and future-ready enterprises.

Although the incorporation process is now fully online through the MCA portal, navigating documentation, compliance, and post-registration requirements can still be challenging.

If you’re ready to launch or expand your business in India or globally, get in touch with our business experts from OnDemand International.

FAQ’s

How much time does it take to register an Indian company?

If you’re ready with all your documents, you can complete the entire registration process in just 15 days.

Does the owner of the company need to be physically present for company registration?

No, the company’s registration process can be completed online. One must have scanned copies of all the documents at hand.

Where can I register my company in India?

By applying to the Ministry of Corporate Affairs on their official portal.

What if someone has already taken my company name?

You can easily check the MCA records online, and if somebody has already taken your company name, then you just need to choose a new name and get your company’s registration done.

Is there any minimum capital requirement for the company?

No, there is no minimum capital requirement for company registration in India.

How can I check if my company was registered or not?

To check the company’s registration status,

Step 1. Visit the MCA’s official website.

Step 2. Go to the MCA Services tab

Step 3. Click “View Company/LLP Master data”

Step 4. Enter your CIN

Step 5. Finally, check the status of the company to see if it says ‘Registered’.