Overview: Sole Proprietorship

If you’re looking to start your own business and wondering what type of structure would be the easiest and most flexible, a sole proprietorship may be the perfect solution. It’s the simplest and most common form of business ownership, where a single individual is responsible for the business’s operations, decisions, and profits.

In India and many other parts of the world, this business structure is especially attractive due to its ease of setup, low cost, and full control it offers to entrepreneurs.

But before you dive in, it’s important to fully understand the features, registration process, and the potential advantages and drawbacks of running a sole proprietorship.

What is a Sole Proprietorship?

If you’re considering setting up a sole proprietorship in India, you’re likely asking yourself, “What is a sole proprietorship?” Let’s break it down for you.

A sole proprietorship, also known as a sole trader business, is the simplest form of business ownership. In its most basic form, a sole proprietorship is a business owned and operated by a single individual. The owner, known as the proprietor, has full control over the business operations, decisions, and profits.

To give you a clear example: if you own a business and are responsible for its daily operations, you are the sole proprietor. You have the authority to grow your business, make all the decisions, and enjoy the profits it generates.

Of course, there may be times when you seek guidance or help from others, such as family members, friends, or colleagues, but the business remains solely under your control.

One of the main reasons a sole proprietorship is so popular is its ease of setup. Unlike other business structures, such as partnerships or corporations, a sole proprietorship doesn’t require formal registration or legal recognition, making it a quick and straightforward option for many entrepreneurs.

As William R. Basset wisely said, “The one-man control is the best in the world if that man is big enough to manage everything.” This quote reflects the independence and simplicity that a sole proprietorship offers to those ready to take on the responsibility.

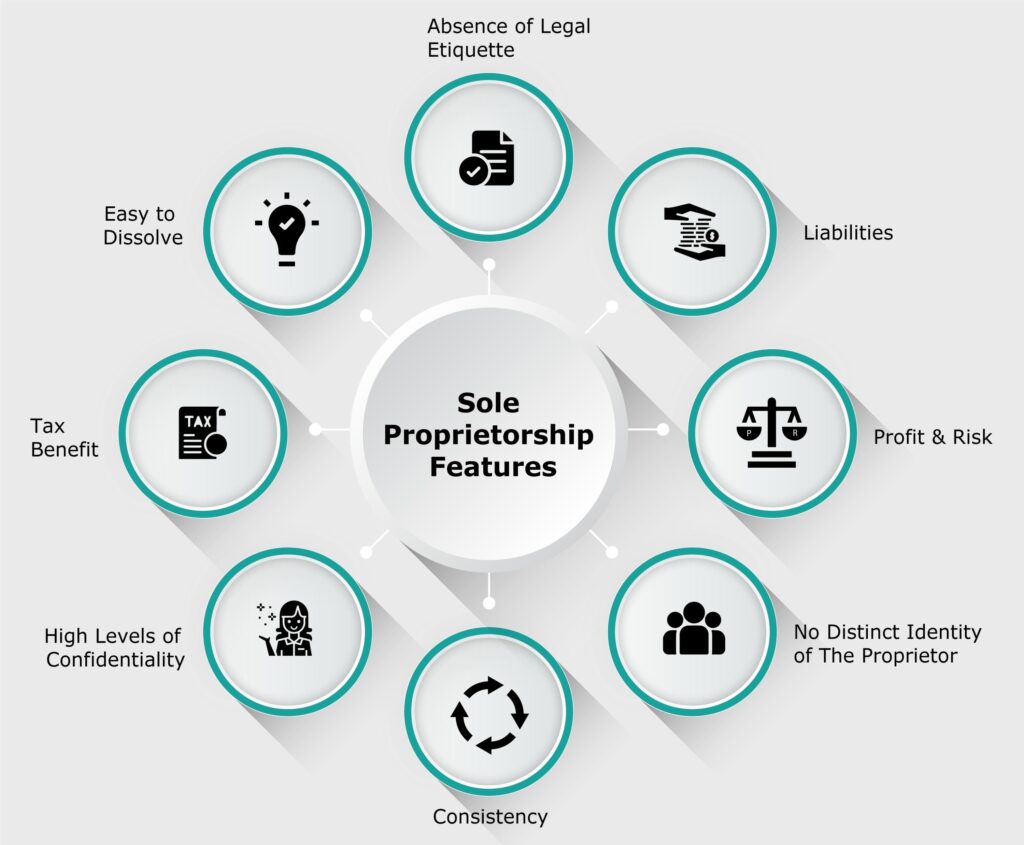

Features of a Sole Proprietorship

A sole proprietorship is one of the most common and straightforward business structures. In this section, we will explore the key features that define a sole proprietorship, helping you understand its advantages and limitations.

1. Absence of Legal Formalities

A sole proprietorship operates without any specific governing law. Unlike other business structures, it does not require separate registration or certification. In most cases, a business license is sufficient to legally operate.

Additionally, dissolving a sole proprietorship is relatively easy, with no complex legal proceedings involved. This makes it a hassle-free option for those looking to start a business quickly.

2. Unlimited Liability

One of the most significant features of a sole proprietorship is unlimited liability. Since there is no legal distinction between the owner and the business, the proprietor is personally liable for all business debts.

In the event of financial failure, the proprietor may have to liquidate personal assets, such as their house or vehicle, to meet business obligations.

3. Profit & Risk

In a sole proprietorship, the owner is both the sole risk bearer and the sole profit recipient. If the business succeeds, the entire profit belongs to the owner.

However, the proprietor also carries the full risk if the business faces losses or failure. This setup means that while the potential for reward is high, the risk is equally significant.

4. No Separate Legal Identity

A sole proprietorship does not have a separate legal identity from its owner. In legal terms, the proprietor and the business are the same entity. This means the owner is responsible for every aspect of the business, including operations, liabilities, and legal obligations.

5. Business Continuity and Succession

Since the sole proprietorship is directly tied to the owner, its continuity is uncertain. Events such as the owner’s death, illness, retirement, or insolvency can result in the dissolution of the business.

Unlike corporations, a sole proprietorship does not have a separate existence, which can make long-term continuity challenging.

6. High Level of Privacy

One major advantage of operating a sole proprietorship is the high level of confidentiality. The business is entirely owned and controlled by the proprietor, meaning all strategies, financial records, and operations remain private.

This confidentiality is beneficial in a competitive market where keeping business information secure is crucial.

7. Tax Benefits

Sole proprietorships enjoy specific tax advantages. Unlike companies, which may be subject to double taxation (corporate tax and dividend tax), a sole proprietor’s income is taxed only once, as part of the individual’s personal income tax.

This simplifies tax processes and may result in lower tax liabilities compared to other business structures.

8. Easy to Dissolve

Another attractive feature of a sole proprietorship is its simplicity when it comes to dissolution. Without partners or co-owners, there are no disputes to settle when the owner decides to close the business.

This flexibility makes a sole proprietorship a great choice for testing new business ideas with minimal risk and commitment.

How to Register a Sole Proprietorship?

Starting a sole proprietorship is relatively easy compared to other business structures.

Here’s a step-by-step guide on how to register a sole proprietorship:

1. Choose a Business Name

The first step is to select a unique business name that represents your venture. You can use your personal name or come up with a creative name.

If you choose a name other than your personal name, ensure it is not already in use by searching with your local business registry.

2. Obtain Necessary Licenses or Permits

Depending on your location and the nature of your business, you may need to obtain licenses or permits to operate legally. This can vary by industry (e.g., food, health, construction) and jurisdiction. Contact your local regulatory authority to find out what’s required.

3. Register Your Business Name (if applicable)

If you decide on a business name other than your personal name, you may need to register it with the appropriate government body. This process is usually straightforward and can be done online in most regions.

4. Apply for an Employer Identification Number (EIN)

While sole proprietorships don’t have to obtain an EIN unless they hire employees, it’s often beneficial to do so. An EIN is needed for tax reporting and helps separate your personal and business finances. You can apply for one online through the IRS or your local tax authority.

5. Open a Business Bank Account

It’s highly recommended to separate your personal and business finances by opening a business bank account. This helps in managing your cash flow, simplifies bookkeeping, and makes tax filing easier.

Also Read: Best Online Bank Account

6. Register for Taxes

Depending on your location, you might need to register for state and local taxes. Ensure you are in compliance with sales tax, payroll taxes (if applicable), and other local business taxes.

Advantages of Sole Proprietorship

Here are some key advantages:

1. Easy to Establish

Compared to other business entities, starting a sole proprietorship is quick and simple. There is minimal paperwork, and registration processes are straightforward.

2. Complete Control and Decision-Making

As the sole owner of the business, you have full control over all business decisions, allowing you to implement ideas and strategies at your own pace.

3. Low Startup Costs

Sole proprietorships typically don’t require expensive legal and registration fees. You can get started with minimal capital, especially if you run an online or home-based business.

4. Tax Benefits

Sole proprietors often enjoy tax advantages, such as pass-through taxation, meaning business profits and losses are reported on their personal tax return. This prevents double taxation that can affect other business structures like corporations.

5. Flexibility in Business Operations

You have the freedom to scale your business operations up or down based on your preferences without the need for shareholder approval or complex agreements.

6. Simple Record-Keeping

Maintaining records and accounts is much simpler in a sole proprietorship. You don’t need to hire an accountant unless your business grows significantly. Just keep track of your earnings and expenses for tax filing purposes.

Disadvantages of Sole Proprietorship

While a sole proprietorship offers many advantages, it’s important to be aware of the potential downsides before making your decision:

1. Unlimited Personal Liability

One of the major drawbacks of a sole proprietorship is that you are personally liable for all debts and legal obligations incurred by the business. This means your personal assets (such as your home or savings) could be at risk if the business faces financial troubles or legal issues.

2. Limited Access to Capital

Sole proprietorships may face difficulties in raising capital because they don’t have the option of issuing stock or attracting investors. If you need funding, you will primarily rely on personal savings or loans, which may limit growth potential.

3. Lack of Business Continuity

A sole proprietorship is tied directly to its owner, which means the business ends if the owner dies, becomes incapacitated, or decides to shut it down. This can make it harder to transfer or sell the business.

4. Limited Expertise

As a sole proprietor, you are responsible for every aspect of the business, from operations to marketing and financial management. While this can be an advantage, it may also limit the ability to leverage external expertise and may stretch your resources thin.

Conclusion

A sole proprietorship offers a straightforward way to start and run a business with minimal formalities, making it an ideal option for small business owners and solo entrepreneurs. The benefits of ease of setup, complete control, and simplified taxes can make it an attractive choice. However, it’s equally important to consider the risks, such as unlimited personal liability and limited access to capital.

Understanding both the pros and cons is crucial to determining if this structure aligns with your business goals.

Are you an entrepreneur looking to open your business internationally? Speak with our incorporation experts from OnDemand International today.

FAQ’s

Is sole trading considered a business?

Sole ownership (also known as a sole trader, single entrepreneur, or just Proprietorship) is an established business owned solely by one person. This is a straightforward type of business structure that is widely used globally.

Shall I establish a Limited Liability Company (LLC) or just a sole proprietorship?

The choice depends on your business size and risk level. Small, low-risk businesses with limited income and a niche customer base (usually initiated as a hobby) are best suited to a sole proprietorship. LLC fits the more risky business with a great growth potential, larger profits, and a requirement to protect its liability and get better tax benefits.

How can I lawfully establish a private company?

It is not difficult to start a Private Company. All you have to do to start a bootstrapped start-up is:

Choose an official name for your company.

Find a suitable site for your company.

Fill out an application for an existing business or government permit.

As a sole proprietor, am I supposed to pay an income to myself?

No. Sole proprietors do not receive a salary. Instead, you take profits from the business. However, you can pay wages to employees if you hire them.

Could there exist a distinction between being self-employed and being a sole trader?

Because they run their firm and do not serve as a worker, a sole owner can be termed self-employed. You are legally considered a self-company owner if you own and operate your own company.

Is it better to start a business as a lone owner or just as a collaboration?

A sole proprietorship lacks enough financing & 3rd party credit options. Partnerships allow a business operator to split financial and operational responsibilities, allowing the company’s smooth growth.

What type of start-ups choose sole proprietorship?

Small local businesses like grocery stores, food vendors, traders, and small manufacturers commonly choose sole proprietorship. It is less suitable for businesses planning large-scale growth.

As a sole owner, how do I file tax returns?

As a single trader, you must complete the usual claim Form for personal taxes, as well as Schedule C, that shows your company’s assets and liabilities. The annual revenue from both is used to quantify the sum of taxes you have to pay.