When you purchase a home in Singapore, you must pay Purchaser’s Income Tax. Furthermore, according to your permanent resident status and the number of residences you possess, you may be required to pay an extra charge called Additional Buyer’s Stamp Duty (ABSD).

What is an Additional Buyer’s Stamp Duty (ABSD)?

It is a governmental fee imposed on the acquisition of two successive residential lands. HDB apartments, domestic retail buildings, mansions, and leased assets are among these holdings. The purchaser’s residence permit has an impact on how additional buyer’s stamp duty is calculated.

ABSD was adopted by the government to make housing values accessible for Singapore residents. They were able to accomplish this by controlling the number of residential buildings. It also attempts to deter immigrants and other organizations from buying numerous homes. The ABSD may be reimbursed by the CPF. The ABSD would have to be paid directly. Perhaps you’ll be able to receive the money from your CPF. Nevertheless, you can only purchase with money from your Conventional Consideration.

Why Was Additional Buyer’s Stamp Duty Introduced In Singapore?

Before we get into the why let’s briefly look into all the changes that have happened regarding the ABSD Singapore:

- Introduced in December 2011 to regulate the demand for properties.

- Rates were first increased introducing a wide range of buyer profiles in January 2013.

- Rates were increased again in July 2018

- Rates were increased again with more diversity-related to foreigners and other entities in December 2021.

The commencement happened in the year 2011. ABSD is also known as a cooling measure by the government of Singapore to keep the properties affordable and discourage foreigners from investing in one or more residential properties. To put it in simple words, ABSD was introduced solely in favor of the Singaporean citizens and to keep the residential property market and its demand regulated.

After the increment in rates in January 2013 introducing a wider range of buyer profiles, it had expected effects. The introduction of ABSD lead to the drop in the property market and well expectedly discouraged foreigners from investing in Singapore properties due to high rates.

Further in time, both BSD and ABSD saw an increase again in the year 2018, and measures like TDSR or Total Debt Servicing Ratio and SSD or Seller’s Stamp Duty saw property transactions have a noticeable drop.

The latest revision and adjustments in the ABSD rates took place in December 2021. The LTV or Loan-to-Value limit for HBD-granted loans saw a tightening dipping it from 90% to 85%. Also, the TDSR or Total Debt Servicing Ratio tightened, essentially dipping a good 5% from 60% to 55%.

ABSD Singapore Rates

ABSD rates are determined by your permanent residency, and the price you’ll have to spend is determined by your citizenship at the date of acquisition. The ABSD proportions in the figures above will apply to either the purchase cost or the marketplace value of the house, whichever one is bigger.

| Profile of the Purchaser | ABSD Payable |

|---|---|

| A Singapore citizen purchases his or her first home. | ABSD is not required to be paid. |

| A Singaporean citizen purchases a second home. | 17% |

| Third and succeeding properties are being purchased by Singapore citizens. | 25% |

| Purchase of a home by a Singapore Permanently Citizen. | 5% |

| Singapore Permanent Residents (PRs) are purchasing second homes. | 25% |

| Purchase of a third and subsequent property by a Singapore Permanent Resident (PR). | 30% |

| Any asset purchased by a foreigner | 30% |

| Organisations (a firm or an organization) that are interested in purchasing an asset | 35% |

Penalties for Late ABSD payment

If ABSD Singapore is not cleared by the timeframe, a Charge Letter will be sent to you, advising you to do the settlement. This message will also notify you of the punishment you will face if you fail to make it on time. Your lender, company, renter, or counsel may be appointed by IRAS to settle the overdue business rates on your account. In the most egregious circumstances, legal proceedings may be pursued to reclaim the debt.

| Payment Delay | Penalties for Late ABSD Payment |

|---|---|

| Payment Delay of up to 3 Months | For late payments of less than three months, a penalty of $10 or the amount due, and see which is greater, will be assessed. |

| Payment Delay of More Than 3 Months | For delayed payment of more than three months, a penalty of $25 or four times the charge collected, whichever is greater, will be levied. |

How To Calculate ABSD Singapore?

As mentioned before, similar to BSD or Buyer’s Stamp Duty, the taxable amount payable is simply based on the valuation of the said property whether it be its purchase price or the market value at the time of the purchase, whichever is deemed to be higher amongst the two. These additional tax rates are often and usually dependent on the buyer’s resident’s status.

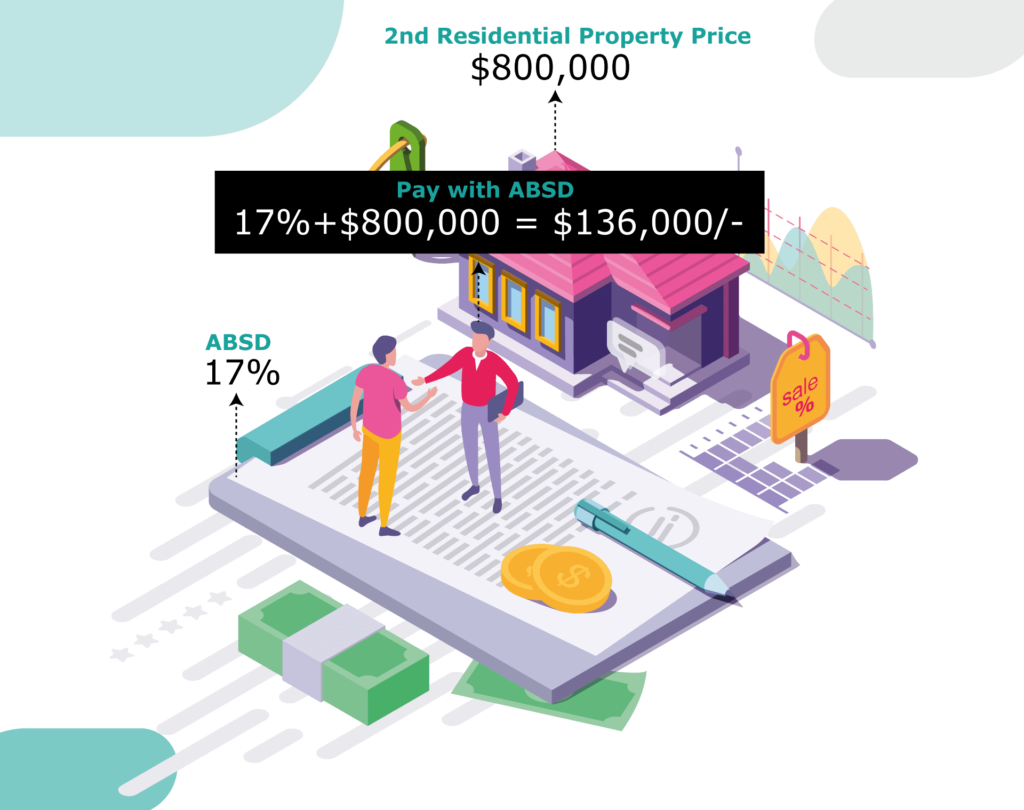

Let us take an example to understand the rates and calculations better:

Say, Otis is a citizen of Singapore and is about to buy her 2nd residential property in Singapore. The property is worth $800,000. Therefore, Otis would pay an ABSD of

17% x $800,000 = $136,000/-

We can see from the above example that Otis or a buyer, in this case, would be required to pay an ABSD of $136,000 on top of its BSD i.e., Buyer’s Stamp Duty.

How To Pay ABSD Singapore?

The Stamp Duty is subjected to be paid within the 14 days of visibility of purchase or sale option, and also from the date of the signed purchase agreement or the date of transfer. It is also a said requirement that both the Stamp Duties (BSD and ABSD) need to be laid in the form of a full installment only and not in partial installments.

Have a look at all the locations to pay the tax and their accepted modes of payment below:

- E-Stamping Portal (online on the web): This location accepts the payment in either eNETS, order of cashier, or a cheque.

- IRAS or Inland Revenue Authority of Singapore Surfing Centre e-Terminals: This location accepts the tax payment in the form of eNET, a cashcard, or NETS.

- SingPost Service Bureaus (located at Chinatown, Novena, Raffles Place, and Shenton Way: This location accepts the tax payment in the forms of cheque, cash, order of cashier, NETS.

The stamping of documents can be done through an online portal via IRAS or the Inland Revenue Authority of Singapore e-Stamping portal. This process also requires the Singpass two-factor authentication (2FA).

What Are The Exemptions In ABSD Singapore?

Of course, there are also a couple of situations where you may not need to pay an ABSD Singapore, like:

- If you have contracted to sell the current residential property before even signing on the Option to Purchase for the new residential property.

- If you are legally downscaling from a bigger private property to a lower HBD resale flat.

Sometimes, it may not be considered an ‘exemption’ per se when a family goes for a dual-key condo unit. This unit is sold as a sole property and therefore, no ABSD is levied. Although no ABSD, these units feature two separate homes comprising a main and sub-unit.

Decoupling is also considered as an exemption sometimes, which is essentially when two co-owners split and transfer their ownership to one of them.

If the buyer is a citizen of Singapore and he/she is married and also in the process of buying their first residential property to live in, they can apply to have the already paid ABSD refunded, even if the other spouse is a foreigner or even a permanent resident.

E.g. A Singaporean husband and his wife who is a foreigner, buy their first residential property together to serve as their marriage home. They would have to essentially pay a 15% Additional Buyer’s Stamp Duty fee (it depends on the status of the wife who is from foreign). They can then seek ABSD remission.

- In the case of particular nationalities:

- The USA

- Norway

- Switzerland

- Iceland

- Liechtenstein

It is because of the Free Trade Agreement, that the permanent residents and nationals of these above-mentioned countries are treated similarly to the Singaporeans. However, permanent residents of the USA aren’t included.

These individuals are treated the same while in the process of acquiring a residential property.

Nationals under the respective FTAs or Free Trade Agreements, permanent citizens and nationals of Liechtenstein, Iceland, Switzerland, Norway, and the USA will be treated similarly to the Singapore Citizens.

Putting it simply, you may not need to pay an ABSD tax for the 1st property purchase. The legal representative on your side can just e-Stamp via the online e-Stamping Portal on the IRAS website to go for the remission.

- In case of the up-gradation of the matrimonial house:

While attempting to go through the enhancement of a marital house, an entity can go for an ABSD remission. But only if another residential property is acquired as a married couple while also selling the first property within the six months of it.

An ABSD remission can be filed for if the residential property is unfinished as well. The catch is that such a remission can only be filed when the first property is set to be sold within six months of the CSC (Certificate of Statutory Compliance) / TOP (Temporary Occupation Permit.Although, you must have kept in check and refrained from buying any other residential property after the second one in the line.

- In the case of developers:

You can simply apply for an ABSD remission if you are purchasing residential land or property and developing four or fewer residential units from the bunch.

What is Buyer’s Stamp Duty?

BSD or State Duty is a tax that is paid on documents that are signed on whenever you decide to buy, acquire or purchase a property that is located in Singapore. Understanding the BSD would also help us in understanding the general difference between the BSD and ABSD.

Also Read: Stamp Duties in Singapore

Who must pay the Buyer’s Stamp Duty?

Any buyer of a specific property is deemed to be liable to pay the assigned Buyer’s Stamp Duty (BSD). A couple of examples of such an instance where buying a property makes you liable to pay the BSD are given below. Take a look:

- Through the means of purchasing e.g. agreement of purchases and sales, accepting the option to purchase or sell.

- Through the means of gifting. A gift, which would include a voluntarily signed trust deed or declaration of trust and settlement.

Trust Deed or Declaration of Trust:

A chargeable fixed duty amounting to $10 is compulsorily payable on the Trust deed/Declaration of Trust. Note that this deed doesn’t result in any change to the benefiting interest in the purchased property.

When and if there is an occurrence of a change in the benefiting interest in the property, the above-mentioned full stamp duty (i.e. SSD, BSD, and ABSD whichever that may be applicable) is liable to be paid on the Trust Deed/Declaration of Trust.

- Through the means of distribution in a species upon the alleged winding up/closing of a company.

- Through the means of distributing from the estate of any deceased individual that isn’t necessarily according to the Will of Intestate Succession Act or the Muslim Law of Inheritance.

What are the rates for Buyer’s Stamp Duty in Singapore?

As we know that every property buyer in Singapore has to pay the BSD. There is no running away. This is more like a tax on your own home that you cannot simply avoid.

Unlike ABSD, the BSD rates have to be calculated solely based upon the value property holds, just as follows:

The market value or purchase price of the property goes into three categories.

- Firstly it is for $180,000. In this, the rates for residential properties remain at 1% and the rates for non-residential properties remain at 1% as well.

- Second, it is like the previous one at $180,000. In this, the rates for both residential and non-residential properties are at 2% each.

- The third category takes the value higher at $640,000. In this, the rates for both residential and non-residential properties remain at 3%.

- Lastly is the remaining amount of the value and the rates for residential property are at 4% in this one and 3% for the non-residential properties.

As you can simply infer from the above information, the more expensive a property you buy, the higher the Buyer’s Stamp Duty Tax you will be liable to pay.

Conclusion

ABSD is an additional expenditure that isn’t changing anytime soon. If you’re searching for ways of avoiding ABSD, make absolutely sure you do your math and think about your options thoroughly so you don’t continue to pay more than you should. For more details contact ODINT Consulting.

FAQ’s

Can I Pay Stamp Duty In Instalments?

No, it is neither allowed nor possible to pay either of the Stamp Duties in Instalments. They need to be paid in one go and a full amount, within 30 days of an effective completion date.

Can the Additional Buyer’s Stamp Duty be paid with CPF? If yes, How?

Yes, it is surely possible and doable to pay the Additional Buyer’s Stamp Duty with CPF. To do so, you and your legal representative will have to make some arrangements with the said CPF Board.

Although, it has been indicated previously that the ABSD is always levied on entities like permanent residents and foreigners but, there is one instance where these entities won’t necessarily need to pay it. So, you’re a permanent resident or a foreigner who is married to a Singaporean, & you also don’t own any residential property there, you won’t be needing to pay any ABSD.

Why property prices are rising in Singapore?

Singapore’s private home or residential property prices have risen at a fast pace within the third quarter, despite the retightened restrictions due to Covid-19, things have been driven by the increasing surge in residential property prices and sales, and the bigger effects from the red-hot Housing Board resale market.

Who pays stamp duty buyer or seller?

The Stamp Duty is liable to be paid by only the buyer of any Singaporean property in most cases. However, it is for both the buyer and the seller that they are supposed to bear the burden of a Stamp Duty Tax for property exchange, purchase, or selling cases. An individual entity who is executing a given instrument can cancel the stamp by writing his/her initials or name across it.

Who is eligible for an ABSD refund?

The refund for the Additional Buyer’s Stamp Duty tax is essentially a special concession that is given only to married Singapore Couples. It helps the couples in facilitating their change of residential properties. For this intent, it is advised that the Couple should sell their first property expeditiously, before jumping onto a second residential property and not remain holding onto two residential properties at the same time.

Who is eligible to claim the ABSD?

Usually, a married couple may or may not be eligible for an ABSD remission on the purchase of a residential property after their marriage. Although, it can only happen if all the conditions for remission under the Stamp Duty (for spouses) Rules are successfully met.

Will the stamp duty be extended for any first-time buyers?

As of now, there have not been any announced plans to make extensions for the buyers of any residential properties in Singapore whether it be for the first time.